After a year of recalibration, the multifamily industry enters 2026 with cautious optimism. In our latest webinar, EliseAI's Andrew Doar sat down with Greg Willett, Chief Economist at LeaseLock, to unpack the forces shaping performance in the year ahead… and we’re bringing you the need-to-know takeaways from that session.

The headline? 2026 may finally deliver on the promise that 2025 couldn't keep.

(Want to watch the full recording? Find it here.)

.svg)

The Setup: Why 2025 Fell Short

Many operators expected 2025 to be a turning point—supply would ease, rents would stabilize, and fundamentals would normalize. It felt like all we heard at conferences in 2024 was “survive until ‘25,” but the reality proved slightly messier. While the first half of the year brought strong leasing activity and early signs of pricing traction, demand cooled sharply in the back half— forcing operators into aggressive concession strategies to fill units, effectively creating an environment where “buying occupancy” was expected.

That pattern may reverse in 2026. With so many leases signed during early 2025's strong market, a wave of renewals will hit in the first months of the new year… right as economists predict lackluster economic growth. With that in mind, we expect the first half of 2026 to be a grind, with momentum building toward the back half as supply pressures continue to ease.

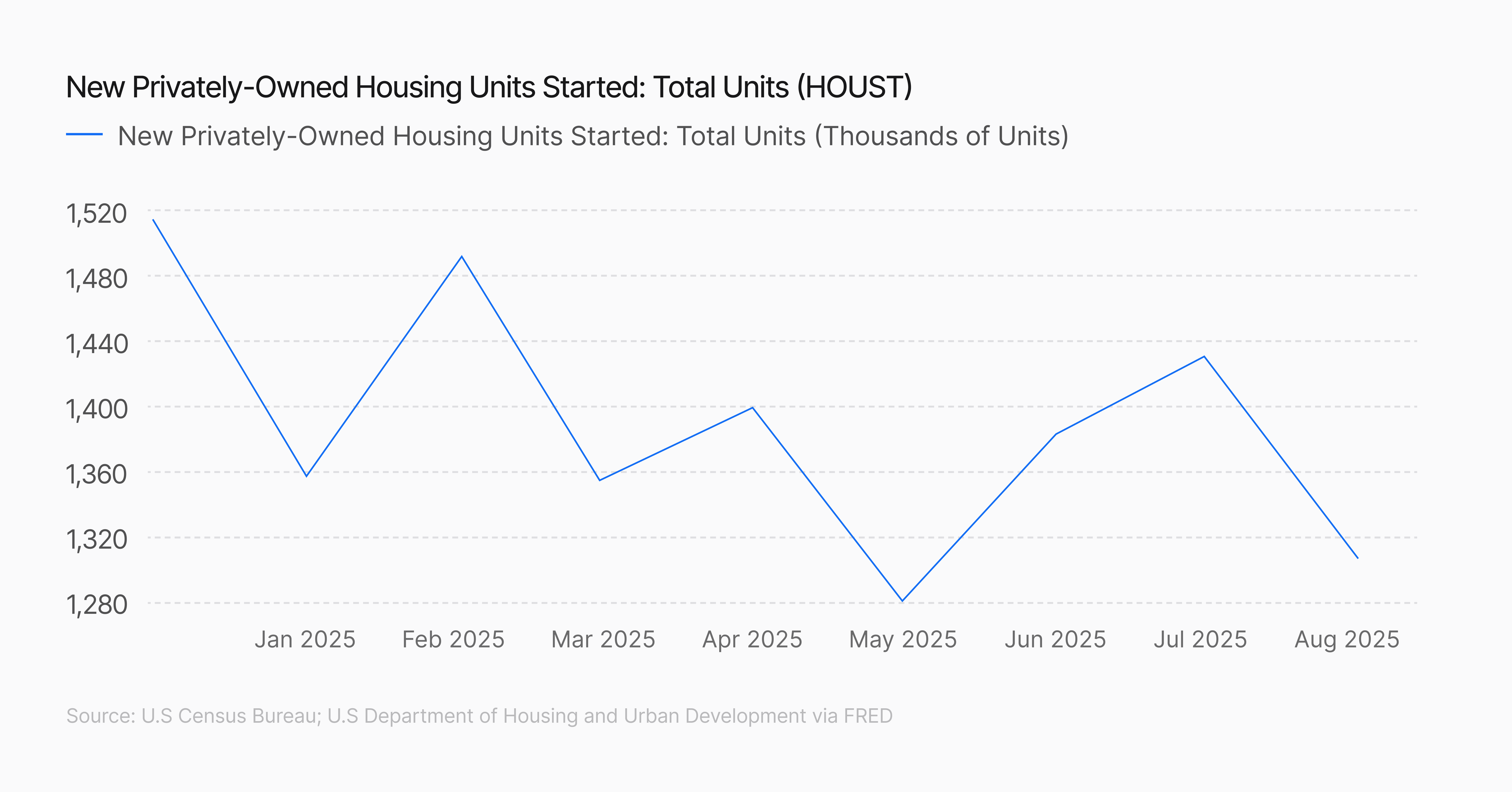

Supply: Still Digesting

Yes, you can start to breathe a little easier—new deliveries are declining from the peak post-pandemic glut we felt in 2024. The roughly 300,000 units expected to complete in 2026 represents a meaningful drop from peak levels. But context matters: while a decrease from a time of pent up demand, that figure still matches pre-COVID norms from 2014-2019. We're returning to normal, not necessarily entering an undersupplied market.

More importantly, the industry still hasn't absorbed the product that came online during the 2023-2025 surge. The fact that completions are slowing down hasn't made the leasing environment any easier, so if you're on-site trying to fill this product, you're still facing the same challenges.

Our expectation? Real supply relief arrives in 2027 and 2028, when today's depressed starts numbers (as a result of general economic insecurity + prohibitive cost of borrowing) translate to genuinely modest delivery volumes.

Demand: The Real Variable

While supply is predictable, demand has become the wild card. The macroeconomic picture introduces uncertainty that wasn't part of the 2026 outlook just months ago.

Consumer finances are the crux of the issue. Rent-to-income ratios look manageable because wage growth has outpaced rent growth in recent years. But total consumer burden tells a different story. Food, healthcare, transportation—everything else has gotten more expensive. Credit card debt has ballooned, and with high interest rates, monthly debt service is eating into household budgets. While distress shows up last in housing because people make that the top priority, we’re already seeing problematic numbers in credit cards and auto loans—something that bears watching coming out of the holiday season.

For Class C properties especially, this manifests in rising delinquency and collections challenges. The K-shaped recovery is real: Class A product is stabilizing while lower-tier assets face compounding headwinds, including sharp vacancy increases in immigrant-heavy neighborhoods as policy uncertainty drives population movement.

Demographics: A Slower New Normal

Beyond cyclical factors, structural shifts are reshaping the market's ceiling. The U.S. population is aging, working-age population growth is slowing, and 2025 may mark the first year of flat or negative population change. And, with 32.5% of 18 to 34 year olds living at home, we're seeing fewer members of that prime renting demographic in market due to economic pressures. The impact of these trends have been noticeable for the multifamily industry: rents are falling, rather than rising, in large swathes of the US market.

The implication of these stats? Growth is coming, but it will be meaningfully slower than previous cycles. Operators should calibrate their expectations accordingly—this isn't the year where you can bake 7% rent growth into your bottom line to shore up any issues your portfolios may be facing.

Markets to Watch

Despite much prognostication that the Sunbelt’s recovery will be challenging, our key takeaway was that the Sunbelt is the region where 2026's story will be written. Not necessarily because these markets will lead the nation in performance, but because they'll show the most dramatic improvement from their recent (and much discussed) troughs.

Austin and Denver, which have seen annual rent cuts around 7%, could moderate to negative 2-3%—a meaningful shift even if technically still declining. Atlanta, Dallas, and the Carolinas are further along, with "green shoots" visible in select neighborhoods that could return to actual growth. While the Sunbelt hasn't quite managed to shake off its post-pandemic malaise, signs are beginning to show that better times may yet be ahead.

Retention: The Critical Metric

With new lease demand uncertain, resident retention becomes the ballast that steadies 2026 performance. Renewal rates remain at historic highs, driven by a combination of economic uncertainty (renters freezing in place due to expensive costs to purchase a home) and deliberate operator investment in the renewal experience.

If retention stumbles, all other rent growth and occupancy problems are exacerbated. The good news: operators who have centralized their renewal process and focused on resident relationships are seeing results. The question is how much of today's strong retention stems from strategic excellence versus renters simply being too nervous to move.

The Bottom Line

2026 won't be a breakout year, but it should mark genuine stabilization after several years of volatility. The first half will test operators as lease expirations stack up against a cautious economic backdrop. The second half offers more room for optimism as supply pressures continue their slow retreat.

The operators best positioned for the year ahead are those who can hold the line on retention, stay disciplined on pricing without leaving money on the table, and maintain operational efficiency as the industry adjusts to structurally lower growth expectations. And the operators who are best positioned to suceed are using EliseAI to improve leasing velocity, reduce bad debt, increase renewal rates, and strengthen their operating efficiency—get in touch with us today to learn more about how EliseAI can help you realize meaningful NOI gains at your assets.