Built to Automate & Scale Your Operations

Answer a couple of questions and we'll connect you with the right team member.

Answer a couple of questions and we'll connect you with the right team member.

Year Over Year Rent Growth (2025)

Apartment Starts in August '25

Expected New Deliveries (2025)

You could say it's an interesting time to be in the apartment business. Perhaps never before has there been such long-term bullishness coupled with so much short-term nervousness.

On the one hand, there's a ton of long-term optimism:

—Multifamily remains the golden asset class in commercial real estate. Investors are more bullish on apartments than any other CRE asset type and plan to increase exposure to the sector, according to a recent survey by John Burns Research & Consulting and CRE Daily.

—There's a growing consensus that apartments are positioned for a strong rebound as the tidal wave of new supply finally subsides.

—Apartment demand continues to come in at some of the highest levels in recent history.

—Resident turnover is very low. And the discount to rent versus buy remains at historic highs, which could keep renters renting longer going forward, too.

—Affordability continues to improve, with wage growth outpacing new lease rent growth for two-and-a-half years.

But despite all the macro tailwinds, it's not all sunshine and rainbows for apartment owners and managers right now. There are very real headwinds, too:

—It's a hyper competitive leasing environment in much of the country thanks to the largest wave of new apartment supply in 40+ years, putting downward pressure on occupancy rates, rents and revenue.

—Discounting is more widespread than usual, and concession values in some markets top more than "one month free" even among stabilized properties not in lease-up.

—New lease rent growth has been flat-ish nationally for two years. Rents continue to fall in especially high-supplied markets.

—Many properties are facing financial challenges tied to today's higher interest rates, and those challenges are compounded by weaker-than-expected revenue.

—Expenses are growing faster than revenues for many groups. While expense pressures have mitigated, there's still a hyper focus on expense control.

Most are likely to be shorter-term challenges, but that's no silver lining for operators trying to hit budget targets they're accountable for. This guide will outline the state of the current market, provide some context on where the road might go from here, and offer strategies for navigating short-term challenges without losing sight of long-term opportunities.

It's all about supply and demand.

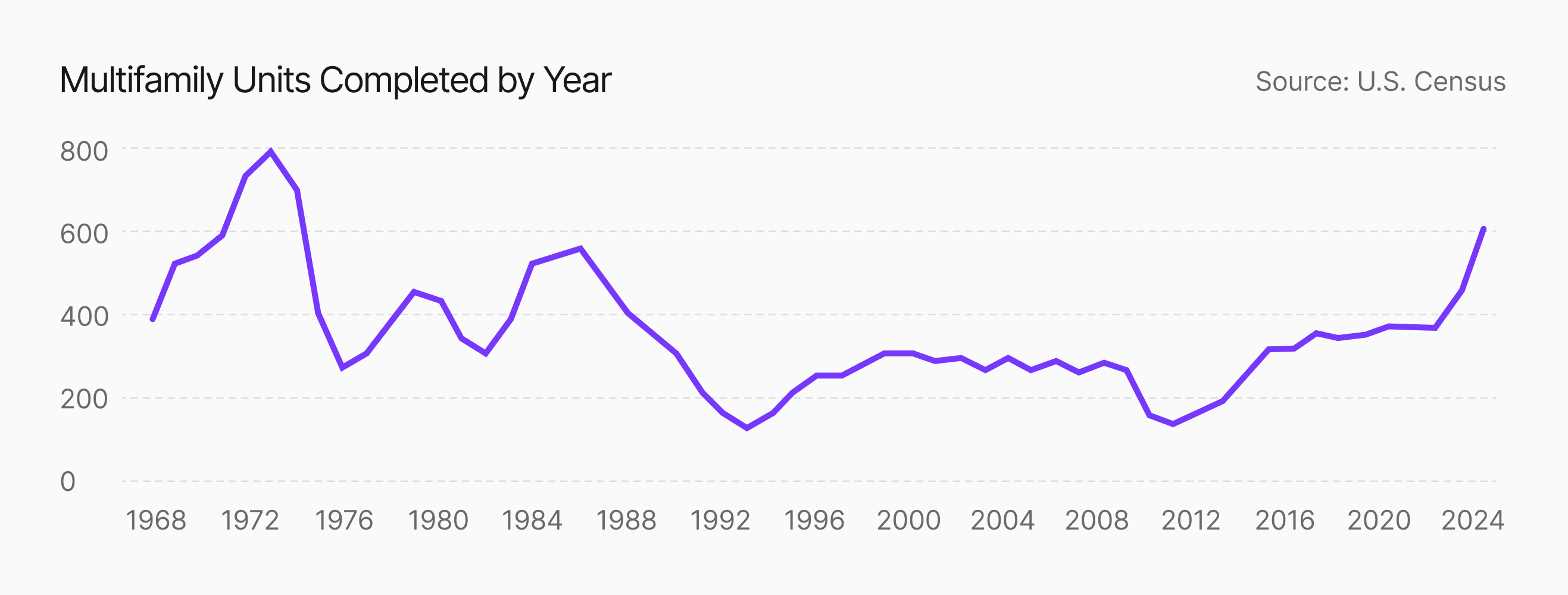

In the second half of the 2010s decade, the apartment market had become steady and somewhat predictable. As the economy chugged along, demand held strong as apartment supply consistently came in around 350,000 units annually and rent growth consistently held around 3-4% annually. All that steadiness went away in 2020 for all the reasons we know.

It's been a rollercoaster ride since then. Demand surged in 2021, catapulting occupancy rates, rent growth and apartment sales to the highest levels in decades. Supply then followed. By 2022, construction topped 1 million units – another multi-decade high. That's when the nose of the roller coaster started to point back downhill.

By the second half of 2022, rent growth was rapidly decelerating. By summer 2023, occupancy rates were rapidly coming off those record highs and rent growth had all but evaporated as new lease-ups pounded the market.

That's still the story today. And it's important to note: It's not a demand issue – at least on a macro level. We're seeing very strong net absorption. But not every operator is feeling all of that demand, and for one simple reason: Most of the net new demand is going into all those newly built apartments. That means leasing traffic and occupancy rates at any individual property may not be as strong as the macro numbers would suggest.

Meanwhile, renter turnover has been unusually low. For apartment operators, there's good and bad that goes with that.

The Good: More renewals help protect occupancy rates. It's a tough market to backfill vacancies, so one smart strategy is simply to prioritize the demand already living at your property – your current resident base.

The Bad: More renewals mean fewer people out in the market looking to move between apartments.

Traditionally, most move-outs aren't to buy houses, it's to move to another apartment. So when more residents choose to stay put, that means fewer prospective residents to whom you can lease a vacant unit.

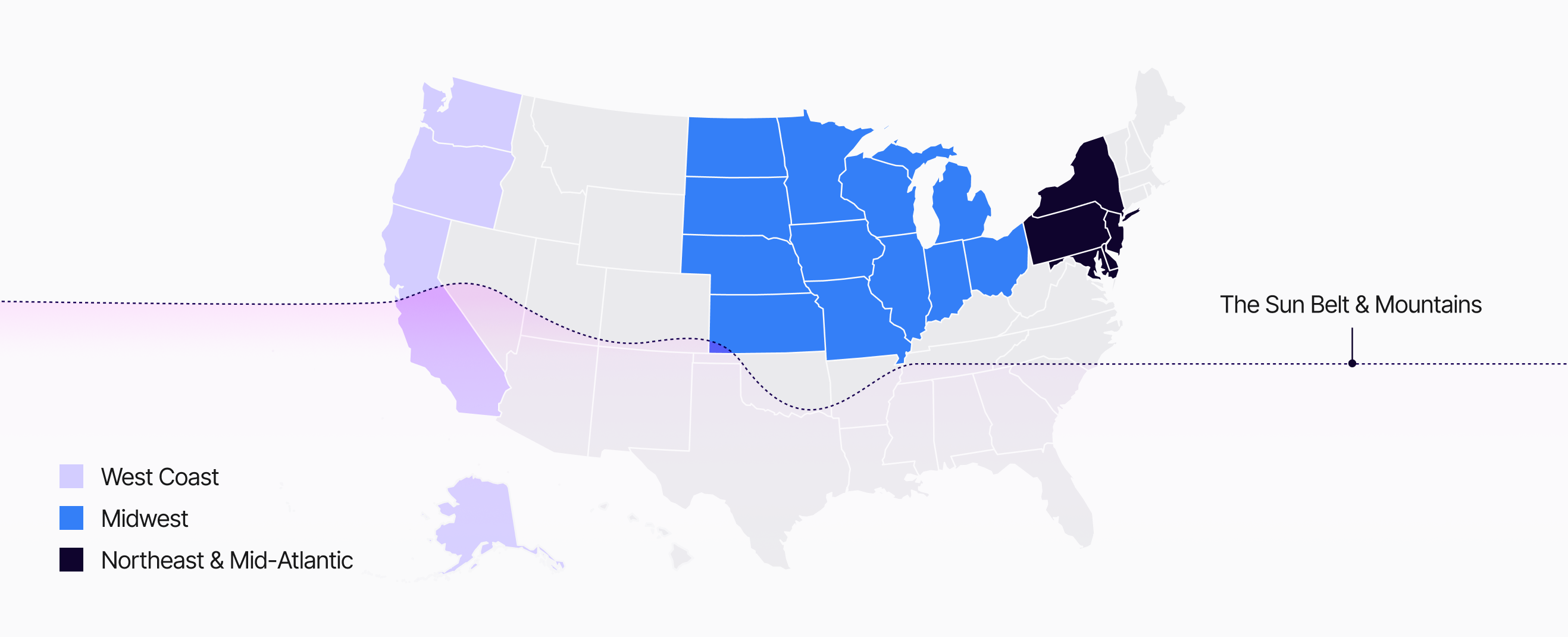

We all know real estate is local, local, local. So while no property or market operates in a vacuum entirely detached from the rest of the country, there are important differences across different parts of the country. It's important to understand those differences and adapt your strategies accordingly, so you're not applying a one-size-fits-all approach.

"Slow and steady" has never been more valued than today, given supply- or regulatory-driven volatility in most of the country these past few years. The Midwest continues to live up to its reputation for low volatility – lower ceiling, but also a lower floor.

Midwest markets have much less new supply ... and relatively little built in the past couple decades, for that matter. Lesser supply plus steady demand has equaled consistently steady rent growth.

Midwest markets have routinely ranked among the nation's rent growth leaders in recent years. Not with double-digit spikes, but with steady increases in the mid-single-digit range as markets elsewhere have cooled down. Top performers include Chicago, Kansas City, Cincinnati, Milwaukee, Columbus, Cleveland and Indianapolis.

Of course, there's also less institutional-grade apartment product in much of the Midwest. That is changing somewhat as more national groups target the Midwest, particularly in the top-end submarkets.

Outside of the Midwest, the Northeast & Mid-Atlantic have been some of the steadiest markets in the country and for similar reasons: Solid demand plus limited new supply. In particular, we've seen strength in key suburbs of New York City (and into Northern New Jersey), Boston, and Washington, D.C.

Of course, the nation's capital now has some question marks around it due to federal layoffs and DOGE cutbacks. So far, the apartment market has held up in terms of demand and occupancy rates. But we've recently seen some softening in retention rates and in rent growth, so this will be a market to watch in coming months.

The West Coast is a bit unique because there's generally been limited supply (though with some key exceptions), but the region has still had challenges due to quality-of-life issues as well as regulatory headwinds. That's limited revenue growth across much of the region in recent years.

More recently, the San Francisco Bay Area has shown signs of rebounding. While rents there remain below pre-pandemic highs, it's now trending in the right direction as quality-of-life issues improve and more workers return to the office.

Southern California remains more of a mixed bag. Los Angeles remains a tough market for operators, but Orange County, Riverside and San Diego have been moderately better. Seattle is a market that does have supply pressures, particularly in the urban core and in some key suburbs – putting downward pressure on rent and occupancy.

The Sun Belt has taken outsized attention in recent years. First: It was the pandemic boom, with accelerated migration into the region driving up demand for apartments and single-family homes. Then it was the supply boom that followed, pushing down rents.

While the supply peak has passed, lease-up competition remains at peak levels. It's taking longer to get new properties leased up, and getting there often requires not only concessions but also base rent cuts.

The competition is real. And it extends into the stabilized market as well. In higher-supplied markets, operators have been hit by the "filtering" effect. That's the process of new properties drawing in higher-income renters from Class A- properties, which then pull renters out of B+ properties, which then pull renters from B-/C+ properties, and down the line. So it's a tough leasing environment even for apartments with rents far cheaper than today's lease-ups. Ultimately that's a win for communities and for renters, but it's a tough reality for apartment owners and managers. Rents have fallen across all asset classes in many markets across this region.

That said, don't assume every Sun Belt market is the same. While it's a tough environment nearly everywhere, some are better positioned for a quicker recovery than others. Markets with strong demand and only modest rent cuts (or even modestly positive growth) right now include Dallas, Houston, South Florida, Tampa and Charlotte.

More challenged markets likely to face prolonged recovery period include Austin, Denver, Phoenix and San Antonio. Note that in many markets, the rebound will be very submarket-specific. For example, in Phoenix, the west side of the market faces far more intense supply pressures than east side. And in Nashville, the suburbs appear primed to rebound faster than the urban core.

At the peak of inflation a few years ago, some apartment owners were seeing OpEx increases in the double-digits. Much of that was fueled by uncontrollable expenses like property taxes and insurance. But payroll also spiked, as operators spent more to retain and attract top talent in a tight labor market.

There's no doubt expense growth has come down since those days.

However, expense pressures remain as a function of compressed revenue growth.

Payroll remains a big focus area for a couple reasons:

—It's a big piece of the supposedly "controllable" expense category.

—It's still tough to retain and hire top talent.

—That reality continues to spur a push toward driving down – or at least containing – payroll costs through centralization, clustered properties and/or role specialization.

Top operators are pursuing something of a Goldilocks scenario (or at least as close as they can get to it) – driving operational efficiencies while also improving the resident experience. They can't afford cuts that would push out existing residents (which would lead to higher turn costs and vacancy loss) or ding lead generation or conversion. But instead they're aiming for the opposite: Could the right efficiencies, executed well, actually boost the odds of retaining residents and converting leads?

And if you're able to do that, then there's an added benefit: Those are efficiencies you can continue to benefit from even when/if revenue growth rebounds.

I'm often asked for my "crystal ball," and my answer is always the same: The crystal ball is fuzzy these days. There are, of course, no guarantees. But we do have clues and probabilities. And that gets us back to supply and demand.

Rent growth levels and occupancy rates (and in turn, net operating incomes) are soft right now primarily for one reason: We're wrestling with a four-decade peak in new apartment supply nationally, and it's going to take time to work through. But remember that supply is the easiest variable to forecast. And every reliable piece of data tells us construction starts have plunged, and therefore completions will be greatly reduced in 2026-27.

That's a favorable outlook for multifamily investors, even if demand normalizes from today's red-hot levels. So assuming the economy remains in decent shape, there's a good chance that consensus outlook plays out. The outlook is favorable, but property owners and managers still have to get through three key challenges first.

Challenge 1: It's a hyper competitive leasing environment. While peak new supply is now in the rearview mirror, we're still in the middle of peak lease-up competition. And while there's a lot of demand out there, you might not see it at your property if most of that net new demand is going to brand-new units in lease up.

Challenge 2: Apartment renters today have a lot of options due to the record volume of new supply plus above-normal vacancy rates in many markets. That means putting increased emphasis on protecting the backdoor – giving your existing residents every reason to want to stay put unless they're moving outside the area.

Challenge 3: While expense pressures have moderated, operating expenses growth is still outpacing revenue growth for many apartment operators. That means finding ways to operate more efficiently. But be careful because, remember, it's a hyper competitive environment. Any efficiencies can't negatively impact your ability to retain current residents (retention) or sign new residents.

It's all about supply and demand.

In the second half of the 2010s decade, the apartment market had become steady and somewhat predictable. As the economy chugged along, demand held strong as apartment supply consistently came in around 350,000 units annually and rent growth consistently held around 3-4% annually. All that steadiness went away in 2020 for all the reasons we know.

It's been a rollercoaster ride since then. Demand surged in 2021, catapulting occupancy rates, rent growth and apartment sales to the highest levels in decades. Supply then followed. By 2022, construction topped 1 million units – another multi-decade high. That's when the nose of the roller coaster started to point back downhill.

By the second half of 2022, rent growth was rapidly decelerating. By summer 2023, occupancy rates were rapidly coming off those record highs and rent growth had all but evaporated as new lease-ups pounded the market.

That's still the story today. And it's important to note: It's not a demand issue – at least on a macro level. We're seeing very strong net absorption. But not every operator is feeling all of that demand, and for one simple reason: Most of the net new demand is going into all those newly built apartments. That means leasing traffic and occupancy rates at any individual property may not be as strong as the macro numbers would suggest.

Meanwhile, renter turnover has been unusually low. For apartment operators, there's good and bad that goes with that.

The Good: More renewals help protect occupancy rates. It's a tough market to backfill vacancies, so one smart strategy is simply to prioritize the demand already living at your property – your current resident base.

The Bad: More renewals mean fewer people out in the market looking to move between apartments.

Traditionally, most move-outs aren't to buy houses, it's to move to another apartment. So when more residents choose to stay put, that means fewer prospective residents to whom you can lease a vacant unit.

We all know real estate is local, local, local. So while no property or market operates in a vacuum entirely detached from the rest of the country, there are important differences across different parts of the country. It's important to understand those differences and adapt your strategies accordingly, so you're not applying a one-size-fits-all approach.

"Slow and steady" has never been more valued than today, given supply- or regulatory-driven volatility in most of the country these past few years. The Midwest continues to live up to its reputation for low volatility – lower ceiling, but also a lower floor.

Midwest markets have much less new supply ... and relatively little built in the past couple decades, for that matter. Lesser supply plus steady demand has equaled consistently steady rent growth.

Midwest markets have routinely ranked among the nation's rent growth leaders in recent years. Not with double-digit spikes, but with steady increases in the mid-single-digit range as markets elsewhere have cooled down. Top performers include Chicago, Kansas City, Cincinnati, Milwaukee, Columbus, Cleveland and Indianapolis.

Of course, there's also less institutional-grade apartment product in much of the Midwest. That is changing somewhat as more national groups target the Midwest, particularly in the top-end submarkets.

Outside of the Midwest, the Northeast & Mid-Atlantic have been some of the steadiest markets in the country and for similar reasons: Solid demand plus limited new supply. In particular, we've seen strength in key suburbs of New York City (and into Northern New Jersey), Boston, and Washington, D.C.

Of course, the nation's capital now has some question marks around it due to federal layoffs and DOGE cutbacks. So far, the apartment market has held up in terms of demand and occupancy rates. But we've recently seen some softening in retention rates and in rent growth, so this will be a market to watch in coming months.

The West Coast is a bit unique because there's generally been limited supply (though with some key exceptions), but the region has still had challenges due to quality-of-life issues as well as regulatory headwinds. That's limited revenue growth across much of the region in recent years.

More recently, the San Francisco Bay Area has shown signs of rebounding. While rents there remain below pre-pandemic highs, it's now trending in the right direction as quality-of-life issues improve and more workers return to the office.

Southern California remains more of a mixed bag. Los Angeles remains a tough market for operators, but Orange County, Riverside and San Diego have been moderately better. Seattle is a market that does have supply pressures, particularly in the urban core and in some key suburbs – putting downward pressure on rent and occupancy.

The Sun Belt has taken outsized attention in recent years. First: It was the pandemic boom, with accelerated migration into the region driving up demand for apartments and single-family homes. Then it was the supply boom that followed, pushing down rents.

While the supply peak has passed, lease-up competition remains at peak levels. It's taking longer to get new properties leased up, and getting there often requires not only concessions but also base rent cuts.

The competition is real. And it extends into the stabilized market as well. In higher-supplied markets, operators have been hit by the "filtering" effect. That's the process of new properties drawing in higher-income renters from Class A- properties, which then pull renters out of B+ properties, which then pull renters from B-/C+ properties, and down the line. So it's a tough leasing environment even for apartments with rents far cheaper than today's lease-ups. Ultimately that's a win for communities and for renters, but it's a tough reality for apartment owners and managers. Rents have fallen across all asset classes in many markets across this region.

That said, don't assume every Sun Belt market is the same. While it's a tough environment nearly everywhere, some are better positioned for a quicker recovery than others. Markets with strong demand and only modest rent cuts (or even modestly positive growth) right now include Dallas, Houston, South Florida, Tampa and Charlotte.

More challenged markets likely to face prolonged recovery period include Austin, Denver, Phoenix and San Antonio. Note that in many markets, the rebound will be very submarket-specific. For example, in Phoenix, the west side of the market faces far more intense supply pressures than east side. And in Nashville, the suburbs appear primed to rebound faster than the urban core.

At the peak of inflation a few years ago, some apartment owners were seeing OpEx increases in the double-digits. Much of that was fueled by uncontrollable expenses like property taxes and insurance. But payroll also spiked, as operators spent more to retain and attract top talent in a tight labor market.

There's no doubt expense growth has come down since those days.

However, expense pressures remain as a function of compressed revenue growth.

Payroll remains a big focus area for a couple reasons:

—It's a big piece of the supposedly "controllable" expense category.

—It's still tough to retain and hire top talent.

—That reality continues to spur a push toward driving down – or at least containing – payroll costs through centralization, clustered properties and/or role specialization.

Top operators are pursuing something of a Goldilocks scenario (or at least as close as they can get to it) – driving operational efficiencies while also improving the resident experience. They can't afford cuts that would push out existing residents (which would lead to higher turn costs and vacancy loss) or ding lead generation or conversion. But instead they're aiming for the opposite: Could the right efficiencies, executed well, actually boost the odds of retaining residents and converting leads?

And if you're able to do that, then there's an added benefit: Those are efficiencies you can continue to benefit from even when/if revenue growth rebounds.

I'm often asked for my "crystal ball," and my answer is always the same: The crystal ball is fuzzy these days. There are, of course, no guarantees. But we do have clues and probabilities. And that gets us back to supply and demand.

Rent growth levels and occupancy rates (and in turn, net operating incomes) are soft right now primarily for one reason: We're wrestling with a four-decade peak in new apartment supply nationally, and it's going to take time to work through. But remember that supply is the easiest variable to forecast. And every reliable piece of data tells us construction starts have plunged, and therefore completions will be greatly reduced in 2026-27.

That's a favorable outlook for multifamily investors, even if demand normalizes from today's red-hot levels. So assuming the economy remains in decent shape, there's a good chance that consensus outlook plays out. The outlook is favorable, but property owners and managers still have to get through three key challenges first.

Challenge 1: It's a hyper competitive leasing environment. While peak new supply is now in the rearview mirror, we're still in the middle of peak lease-up competition. And while there's a lot of demand out there, you might not see it at your property if most of that net new demand is going to brand-new units in lease up.

Challenge 2: Apartment renters today have a lot of options due to the record volume of new supply plus above-normal vacancy rates in many markets. That means putting increased emphasis on protecting the backdoor – giving your existing residents every reason to want to stay put unless they're moving outside the area.

Challenge 3: While expense pressures have moderated, operating expenses growth is still outpacing revenue growth for many apartment operators. That means finding ways to operate more efficiently. But be careful because, remember, it's a hyper competitive environment. Any efficiencies can't negatively impact your ability to retain current residents (retention) or sign new residents.