Built to Automate & Scale Your Operations

Answer a couple of questions and we'll connect you with the right team member.

Answer a couple of questions and we'll connect you with the right team member.

Of Affordable Operators Have Deployed AI

Of Affordable Operators Are Increasing AI Budgets YOY

Of Affordable Teams Have Restructured Around AI

A third-party conducted survey shows affordable housing operators have matched market-rate operators’ AI adoption rates, with nine in ten deploying AI into their daily operations and nearly three quarters growing their budgetary investment year over year. But what the data reveals is a misalignment. The areas that actually define the complexity of affordable operations, like compliance, recertification, and income verification, are the ones AI adoption faces key challenges. Not because the technology doesn't exist, but because operators aren’t yet confident it was built for their regulatory environment given the higher stakes and complex workflows. They remain largely manual, handled by the same lean teams already carrying more than market-rate peers, with less budget and less margin for error. The bar for trusting AI in these workflows is legitimately higher, and some operators aren't there yet.

This report examines how affordable operators are navigating that gap. Drawing on survey responses from 400 property management professionals (162 of which manage affordable portfolios) and operational insights from conversations with affordable housing teams around the nation, it maps where the industry stands today, where it's headed, and where the largest opportunities remain.

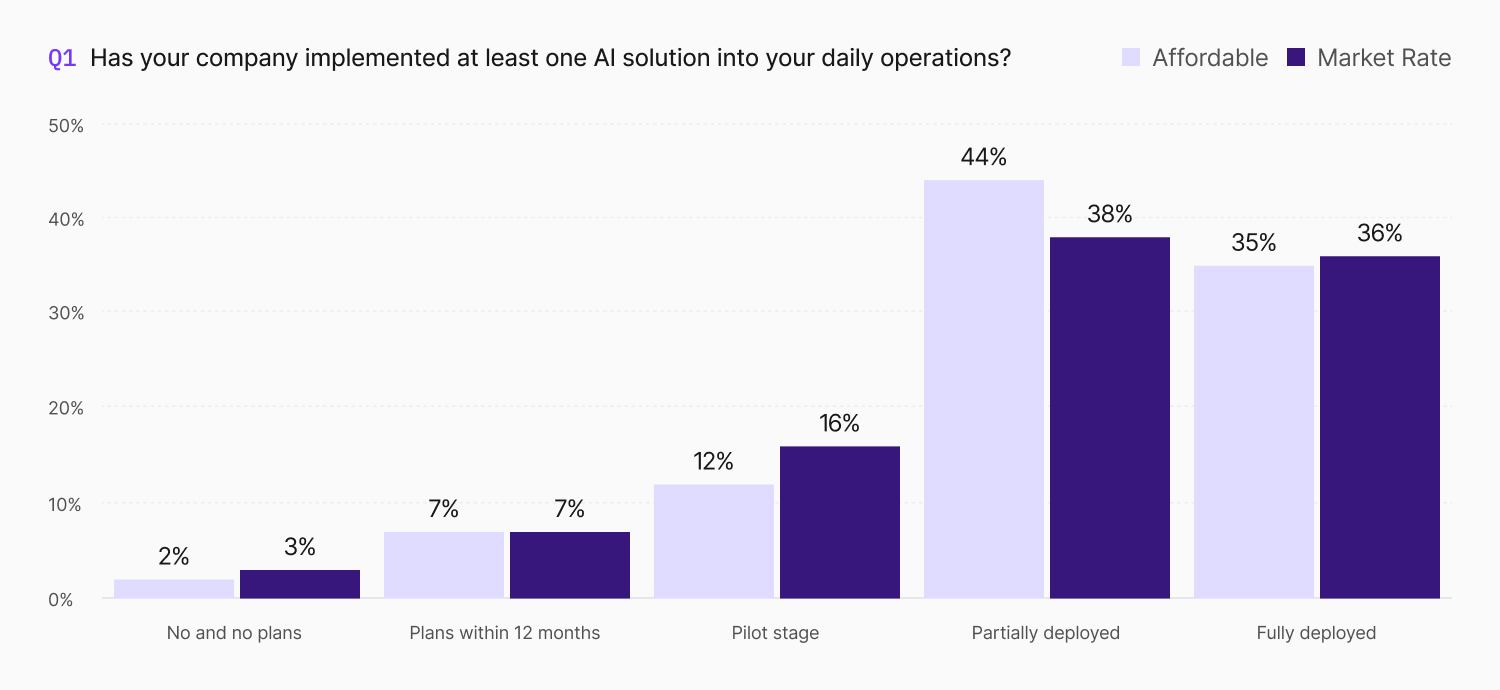

The AI adoption question is closed. 91% percent of the affordable operators we surveyed have implemented at least one AI solution into their daily operations, matching adoption rates across their convention peers. 7% of affordable respondents have plans to implement AI within 12 months and only 2% say they have no plans to implement AI at all. What's worth noting is the pace of that adoption. 44% percent of affordable operators report partial deployment, with another 35% fully deployed, suggesting the industry has moved past the pilot phase and into operationalization. The question is no longer about deploying AI in Affordable, it’s where and what gaps remain?

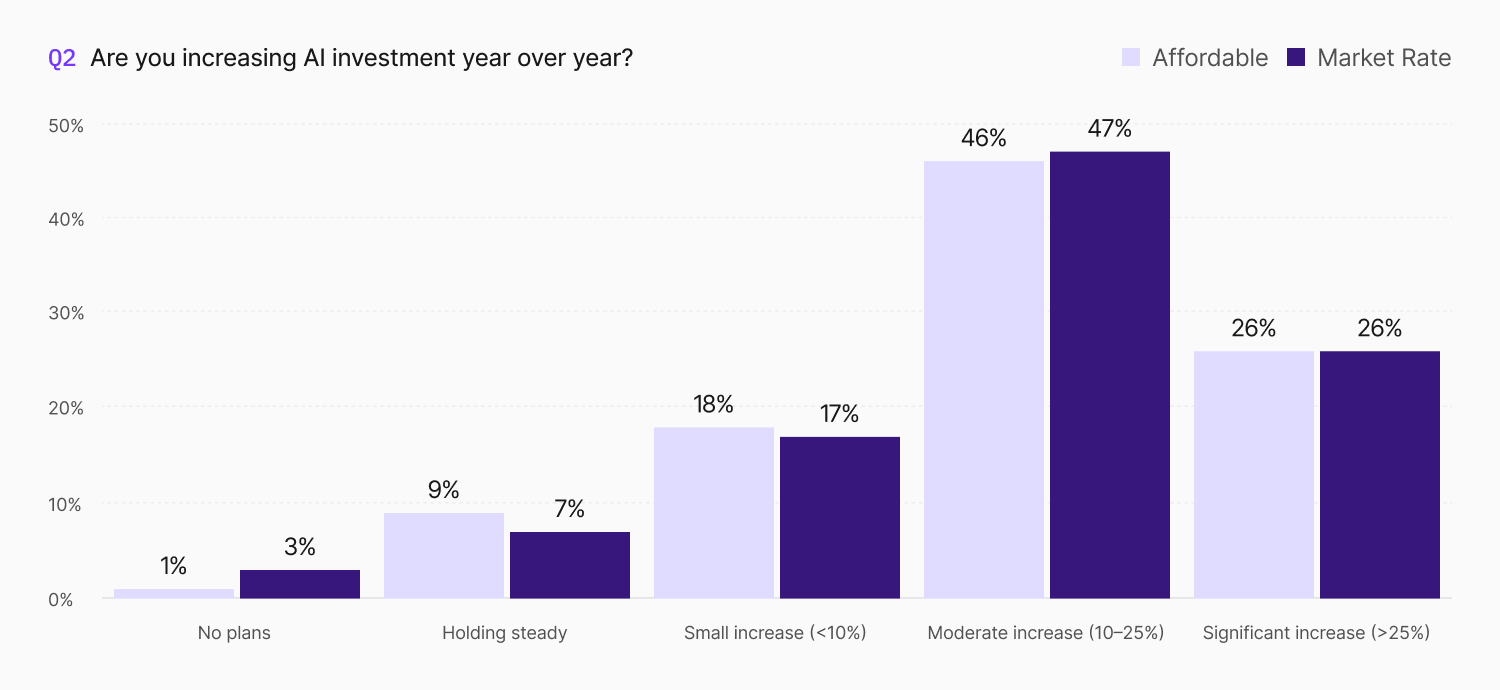

The investment on AI tells the same story. 72% percent of affordable operators are increasing their AI investment by 10% or more year over year, with more than a quarter committing to increases above 25%. The increasing budget allocation indicates that both affordable and market-rate operators are treating AI as core infrastructure, allocating dedicated budgets, planning multi-year rollouts, and embedding these tools into how they staff, train, and evaluate performance.

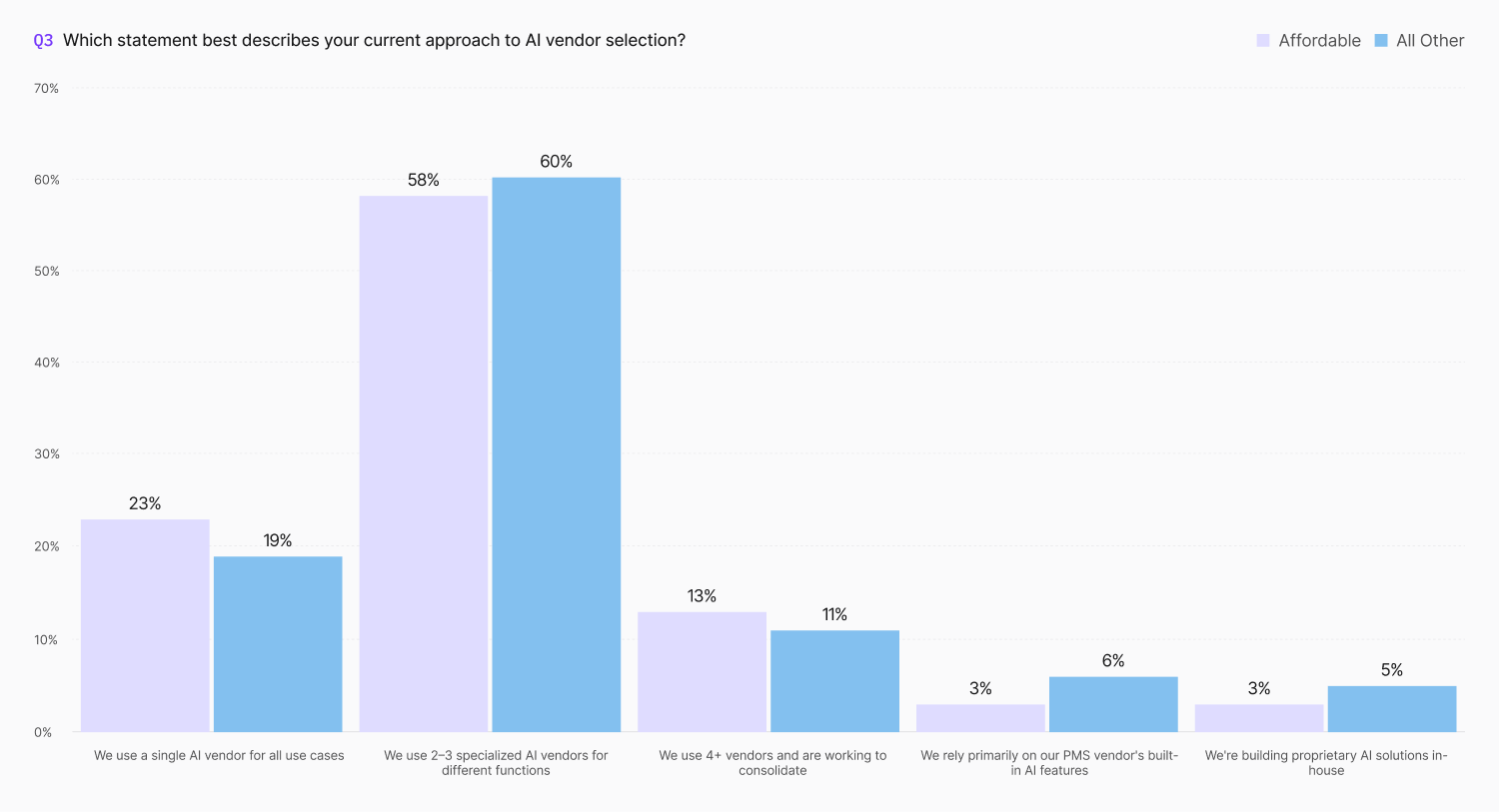

How that budget gets allocated gives us insights into the technology preference of affordable housing operators. 58% of affordable operators today are working with two to three specialized AI vendors for different functions, while only 3% rely primarily on their PMS vendor's built-in AI features. The multi-vendor approach reflects a reality of operating in the affordable housing segment: no single platform has yet delivered end-to-end coverage across affordable housing operations, so operators are assembling best-of-breed stacks that layer specialized tools on top of existing base tools. For affordable operators in particular, this creates opportunity and complexity alike. More tools means more integration work, more vendors to manage, and more pressure to ensure continued compliance across a fragmented technology ecosystem.

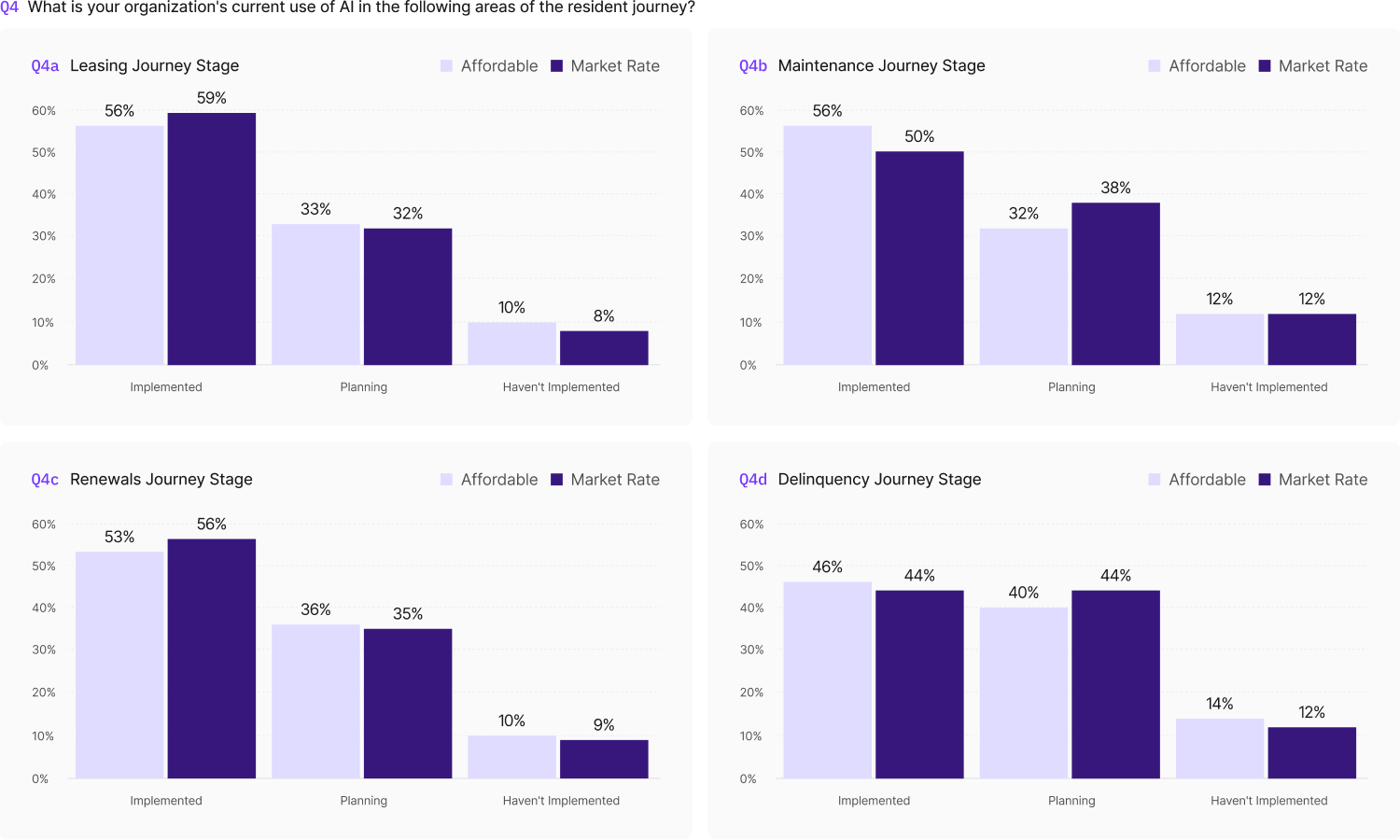

Across the four core operational areas where AI is being deployed today, affordable operators are keeping pace with or outpacing their market-rate peers in almost all areas. Leasing is the most mature category for AI deployment for both segments, with 56% of affordable operators reporting implementation (within three points of market rate). LeasingAI is the lowest friction starting part, with the biggest opportunity to capture unnurtured leads around the clock. However, many of the most operationally complex workflows in affordable housing, including certification, recertification, managing set asides, and waitlist management, remain painstakingly manual, largely pen and paper.

Maintenance is where affordable begins to pull ahead in overall deployment rates, with 56% of surveyed affordable operators deploying AI for maintenance workflows, compared to 50% of market-rate operators. This arguably reflects the outsized pressure affordable teams face in managing high work order volumes with lean staffing, leveraging AI-powered intake, triage, and routing to keep closure percentages high. Renewals too show near-parity, with affordable trailing slightly at 53% versus 56%.

Delinquency is the category with the most forward momentum. Current implementation of delinquency in affordable sits at 46%, the lowest of the four areas, but 40% of those who haven't deployed here yet say they plan to within 12 months. That makes delinquency the clearest next frontier for AI deployment in affordable housing, a trend we’ll explore further later in this report.

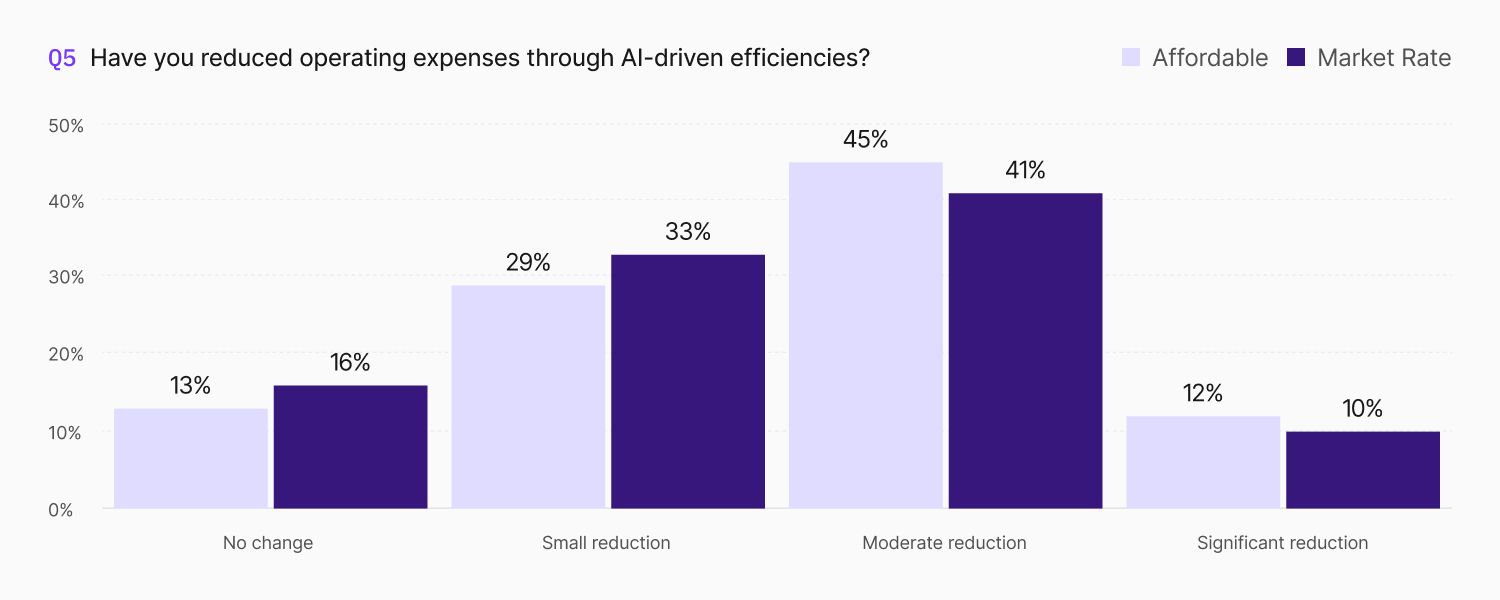

The financial returns are beginning to materialize for the affordable segment. 58% of affordable operators report moderate or significant reductions in operating expenses as a direct result of AI-driven efficiencies, outpacing market-rate operators by seven percentage points. This gap is particularly notable given that affordable operators typically work with tighter margins and less technology budget. The fact that they're seeing stronger expense reductions suggests that the operational baseline they're automating away from was more labor-intensive to begin with. When the starting point involves manual recertification tracking, paper applications, and spreadsheet-based compliance workflows, even targeted automation can help to deliver outsized returns.

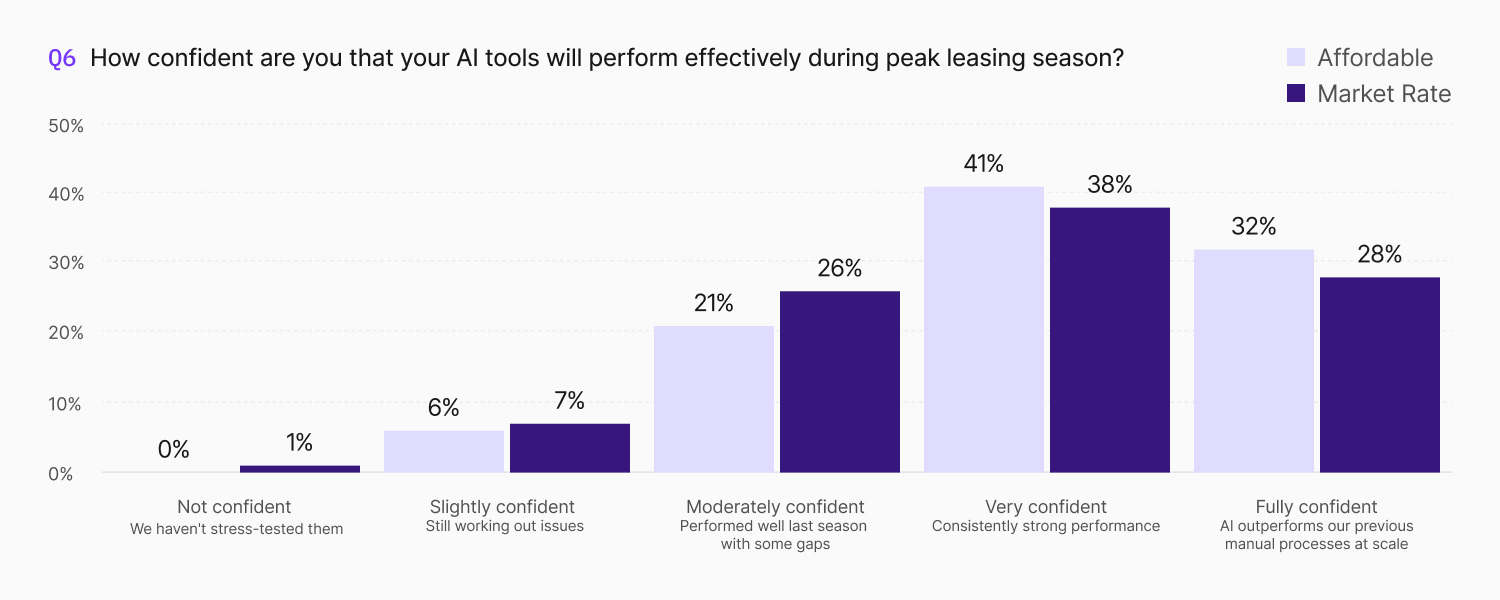

Confidence levels tell a similar story. Nearly three-quarters of affordable operators say they are very or fully confident that their AI tools will perform effectively during peak leasing season, with 32% saying AI now outperforms their previous manual processes at scale. That seven-point confidence gap over market-rate peers likely reflects what happens when AI replaces processes that were already running past capacity. When your baseline is a small team managing compliance, leasing, and resident communication across hundreds of units, the performance bar AI needs to clear looks different than it does for a fully staffed conventional property. Affordable operators are seeing strong results because the need was that much more acute.

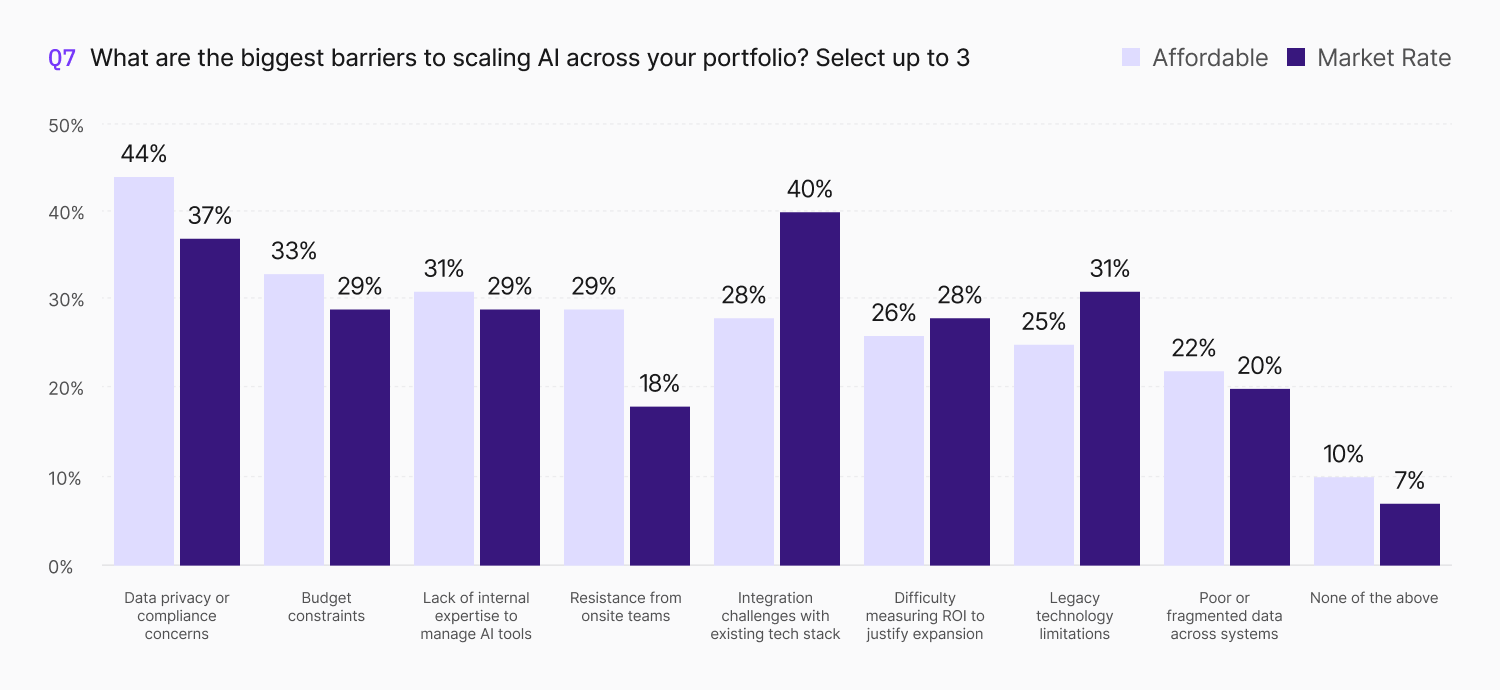

The previous section showed that affordable operators are adopting AI at rates that match or exceed market rate across leasing, maintenance, renewals, and delinquency. But when we ask what's holding them back from going further, some affordable-specific barriers come into focus.

Data privacy and compliance concerns top the list for affordable operators at 44%, seven points above that of their market-rate peers. Affordable operators are astutely asking what data are these models accessing, where is it stored, who reviews the output, and how does the audit trail hold up under a state agency review or HUD inspection.

The second notable gap is onsite team resistance, where affordable operators are 11 percentage points more likely to cite it as a barrier than market-rate operators (29% vs. 18%). This is less about whether staff want new technology to reduce their workload (they do) and more about the conditions under which they're being asked to adopt it (with the aforementioned regulatory complexity). Affordable housing site teams are smaller, and usually carry broader responsibilities across compliance, leasing, and resident services simultaneously. Layering a new tool into an already overloaded workflow creates friction that a larger, more specialized market-rate team may not experience in the same way. The path to adoption starts and ends with thoughtful implementation processes that both account for existing staff capacity and the complexity of the work they're already managing.

Where the data gets interesting is integration challenges. Market-rate operators rank this as their top barrier at 40%, while affordable operators place it lower at 28%. Our hypothesis? Affordable operators, many of whom are still running manual or spreadsheet-based processes for compliance work, have less existing automations to integrate against. The integration challenge assumes you have systems to connect, which, given the budgetary constraints of the affordable segment, often results in less digital infrastructure.

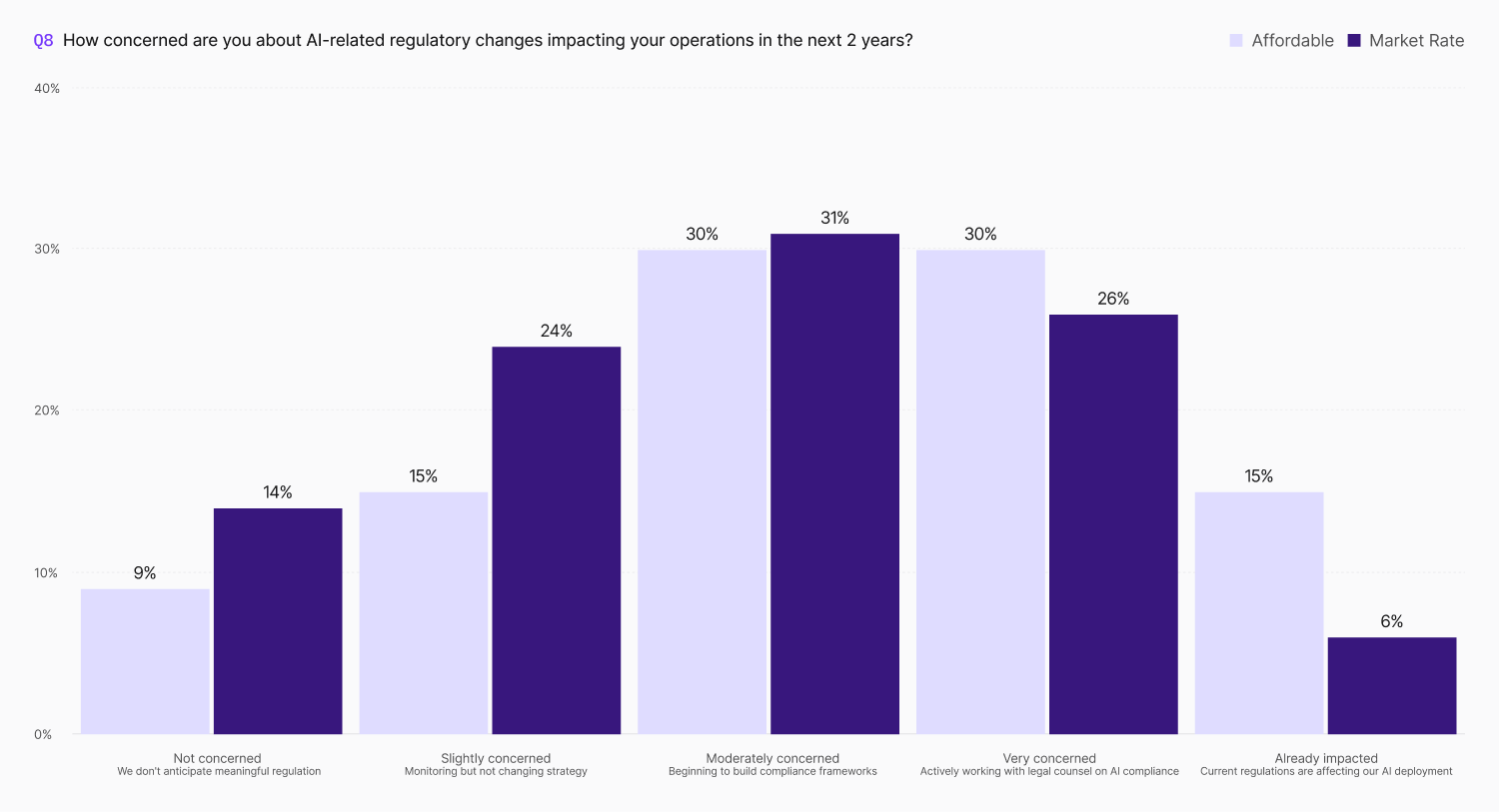

One of the largest gaps in our entire survey between market rate and affordable is about regulatory risk. 46% of affordable operators say they are very concerned or already impacted by AI-related regulatory changes versus 32% of market-rate operators. This 14% gap is the second widest across every question we asked. 15% of affordable operators noted that current regulations are already affecting their AI deployment (roughly two and a half times the market-rate figure), showing the increased compliance focus is already manifesting itself in tech rollouts.

Affordable housing compliance across programs like LIHTC, HUD Section 8, HOME, and Bond demands AI that is auditable, explainable, and defensible under review. The addition of staggered HOTMA implementation requires configurable tools that can manage changing guidance. Most AI tools were not built to manage the layered, ever-changing complexities in affordable housing.

The opportunity this presents is significant. Income certification and recertification are where the most staff time goes and where errors are most expensive, with the potential for loss of millions of dollars in tax credits for a few clerical errors. The operators who close this gap first will outperform on efficiency in ways leasing automation alone can’t deliver. The question is what tool to choose that is built for affordable operators in mind, and how to deploy them properly.

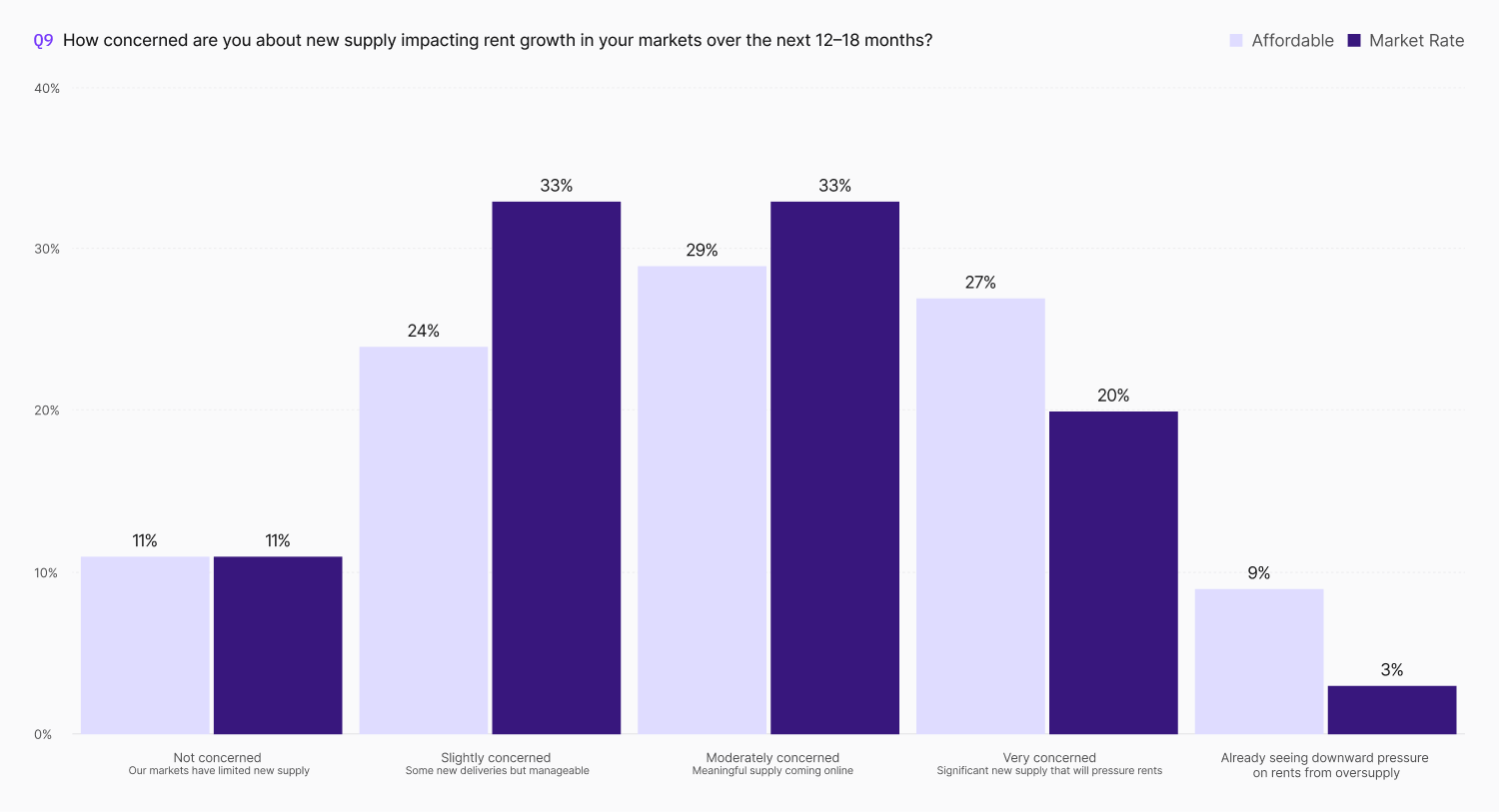

While overall concern levels about new supply are similar across both segments (56% vs. 53% moderately or very concerned), the nature of that concern differs. 9% of affordable operators say they are already seeing downward pressure on rents from oversupply, 3x the market-rate figure. This likely reflects localized LIHTC markets where recent tax credit allocations have concentrated new affordable supply, creating competition among affordable communities in ways that mirror what market-rate operators experience more broadly. In these markets, operational efficiency and resident experience become competitive differentiators in ways they historically haven't been for affordable housing.

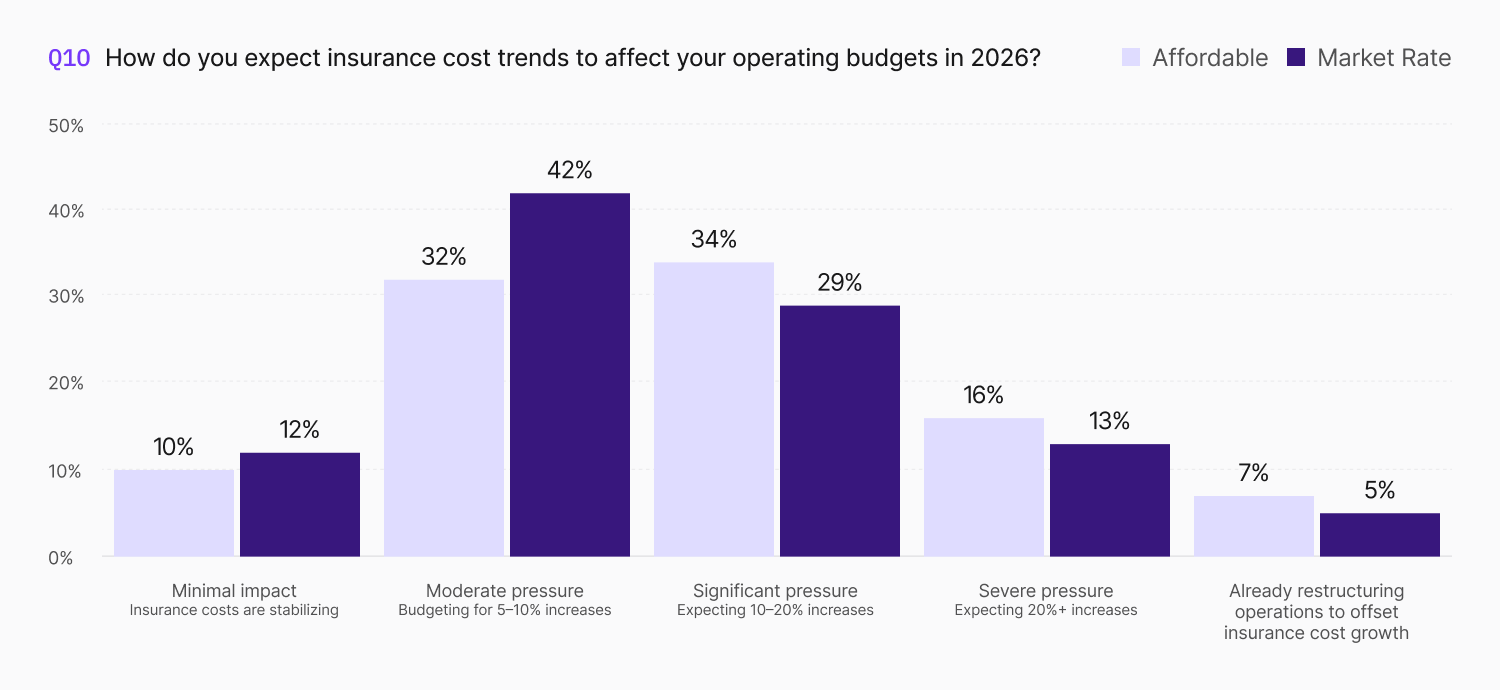

Insurance is adding another layer of financial pressure. Half of affordable operators expect significant or severe insurance cost increases in 2026, eight points above market rate. And while market-rate operators are more concentrated in the moderate pressure band (42% budgeting for 5–10% increases), affordable operators skew toward the higher end, with 16% bracing for increases above 20%. Seven percent say they're already restructuring operations to absorb insurance cost growth.

Insurance pressure compounds differently in the affordable segment, with revenue constraints from regulatory rent caps, HAP payment schedules, and income-based rent calculations leaving less room to pass costs through to residents. When insurance, utilities, and maintenance costs rise, the only lever most affordable operators have is operational efficiency. That reality only accelerates the case for automation and AI as a margin preservation strategy.

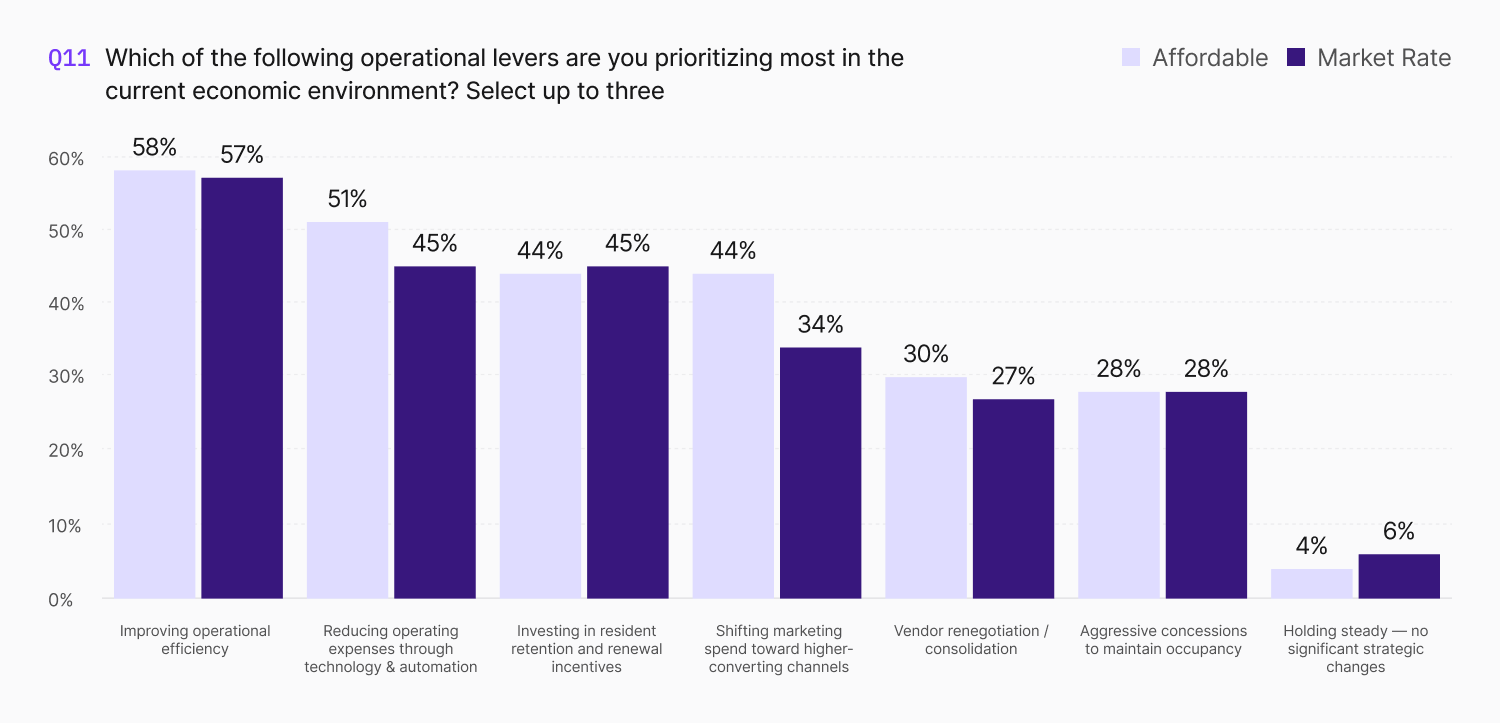

When asked which operational levers they're pulling in response to these pressures, affordable operators are leaning into technology and efficiency at higher rates than their market-rate peers. 51% are prioritizing operating expense reduction through technology and automation, six points above market rate. Only 4% of affordable operators say they're holding steady with no significant strategic changes. The vast majority are actively adjusting how they operate, and technology is central to that adjustment.

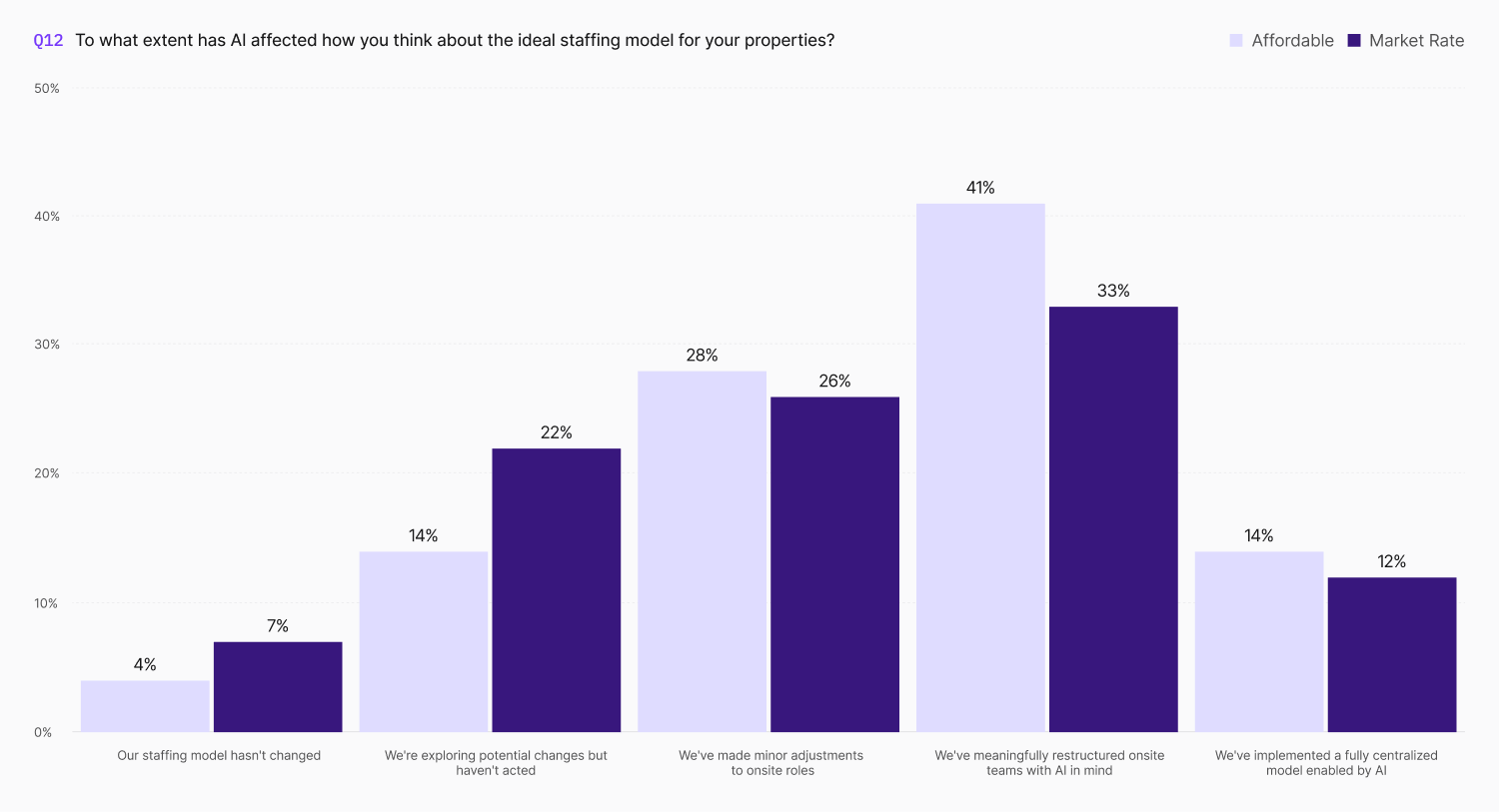

More than half of affordable operators have restructured onsite teams or centralized operations around AI, 10% points above market rate, and this number is expected to grow. The staffing pressure predates AI: lean teams, persistent turnover, and compliance work that makes every new hire expensive. AI provided the mechanism to act on pressure that had been building for years. Routine tasks move to AI so that staff can focus on compliance reviews, hardship conversations, agency reporting.

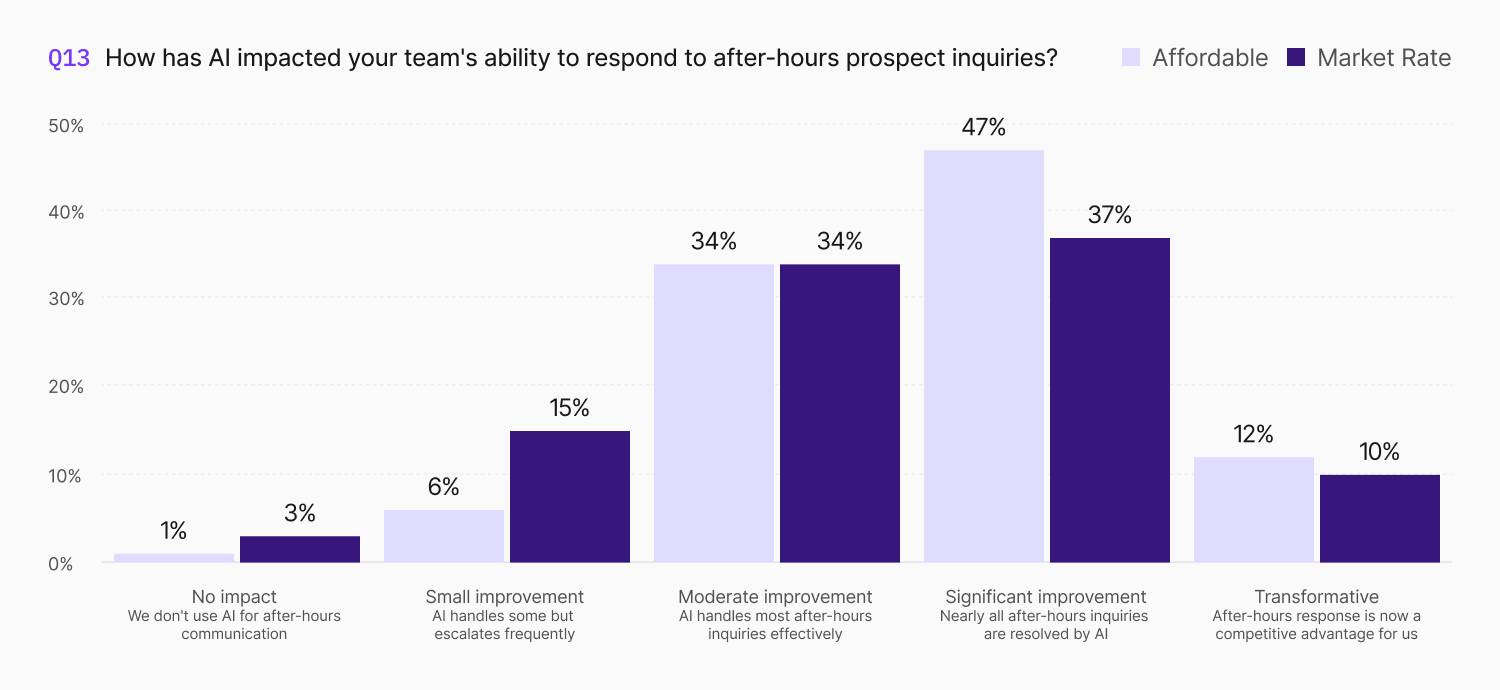

The after-hours data illustrates what this restructuring looks like in practice. 81% of affordable operators report that AI has delivered moderate to transformative improvement in their ability to respond to prospect inquiries outside business hours, 10 points above market rate. Nearly half say that almost all after-hours inquiries are now resolved by AI without staff involvement. This matters disproportionately in affordable housing. Properties with smaller teams and no dedicated after-hours staff were historically dark from 5 PM to 9 AM. AI has effectively extended the operating hours of affordable properties without adding payroll.

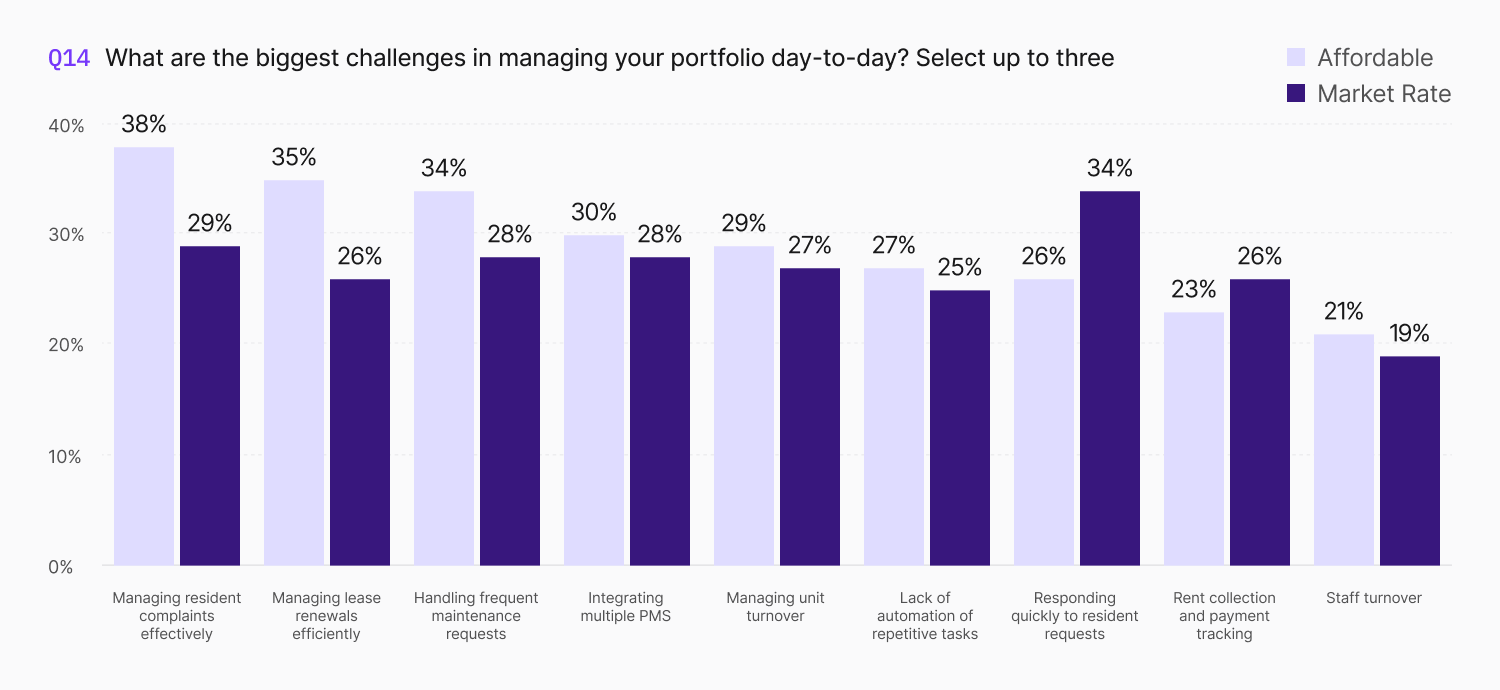

Despite similar AI adoption rates, affordable housing operators consistently report higher challenge levels across resident complaints (38% vs. 29%), managing renewals (35% vs. 26%), and maintenance requests (34% vs. 28%). Automation has not erased the gap because the work is structurally more complex.

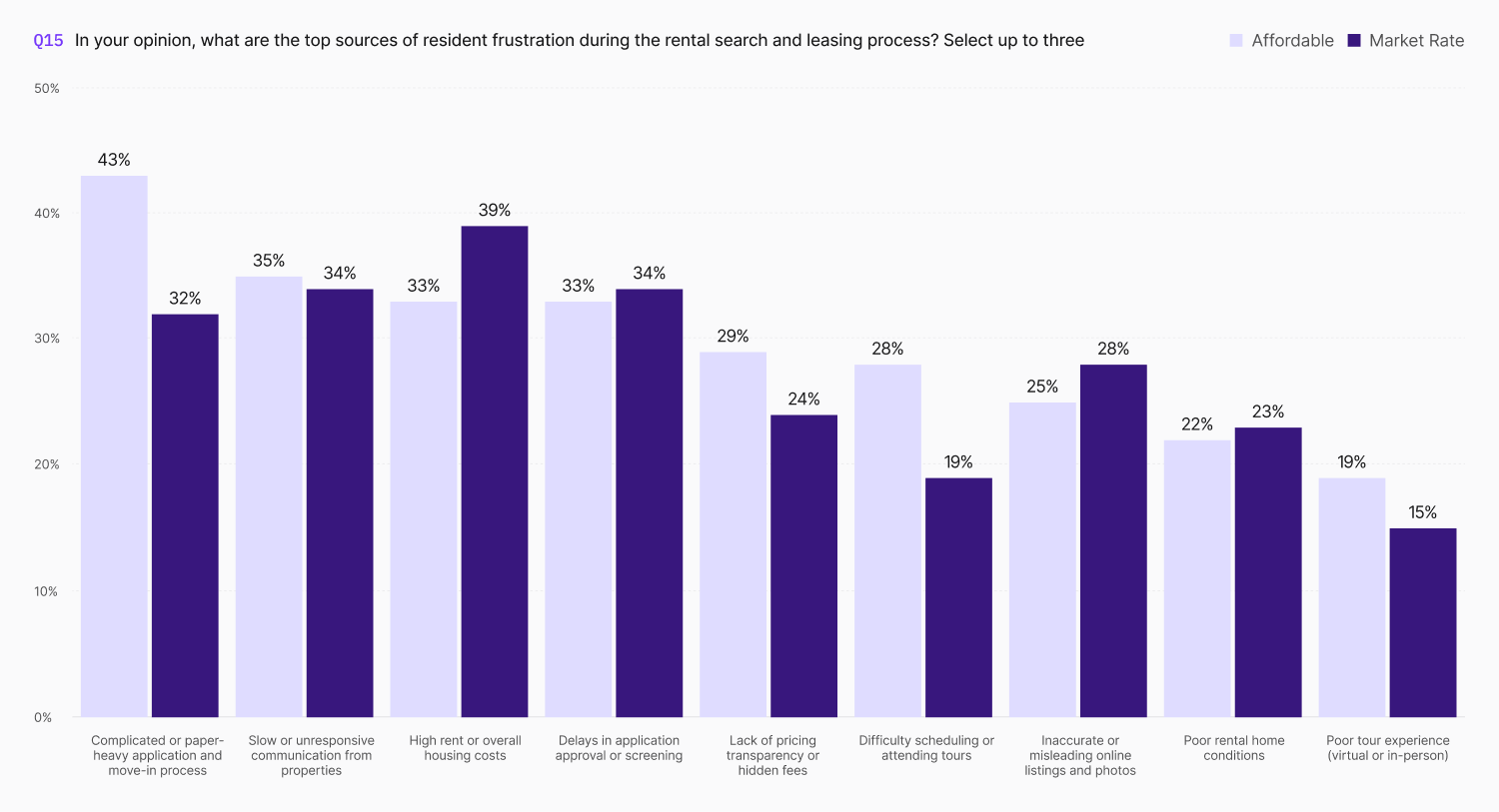

The top source of resident frustration during the affordable rental journey is the application process. Income documentation requirements, eligibility verifications, and program-specific paperwork can stretch the process across days or weeks. Rent cost, which leads the list for market-rate operators at 39%, ranks lower for affordable at 33%. The frustration that defines the affordable prospect experience isn’t price, but application friction. Every additional document, every manual verification step, and every delay in application processing represents a barrier between an eligible household and a unit that's sitting vacant waiting for them.

Tour scheduling difficulty also shows a meaningful gap, which tracks with the staffing realities covered earlier. Smaller site teams with competing compliance and leasing responsibilities have less availability to accommodate tours, particularly for working applicants who need evenings or weekends. AI-assisted scheduling and self-guided tour technology address this directly, but adoption in affordable housing has been slower.

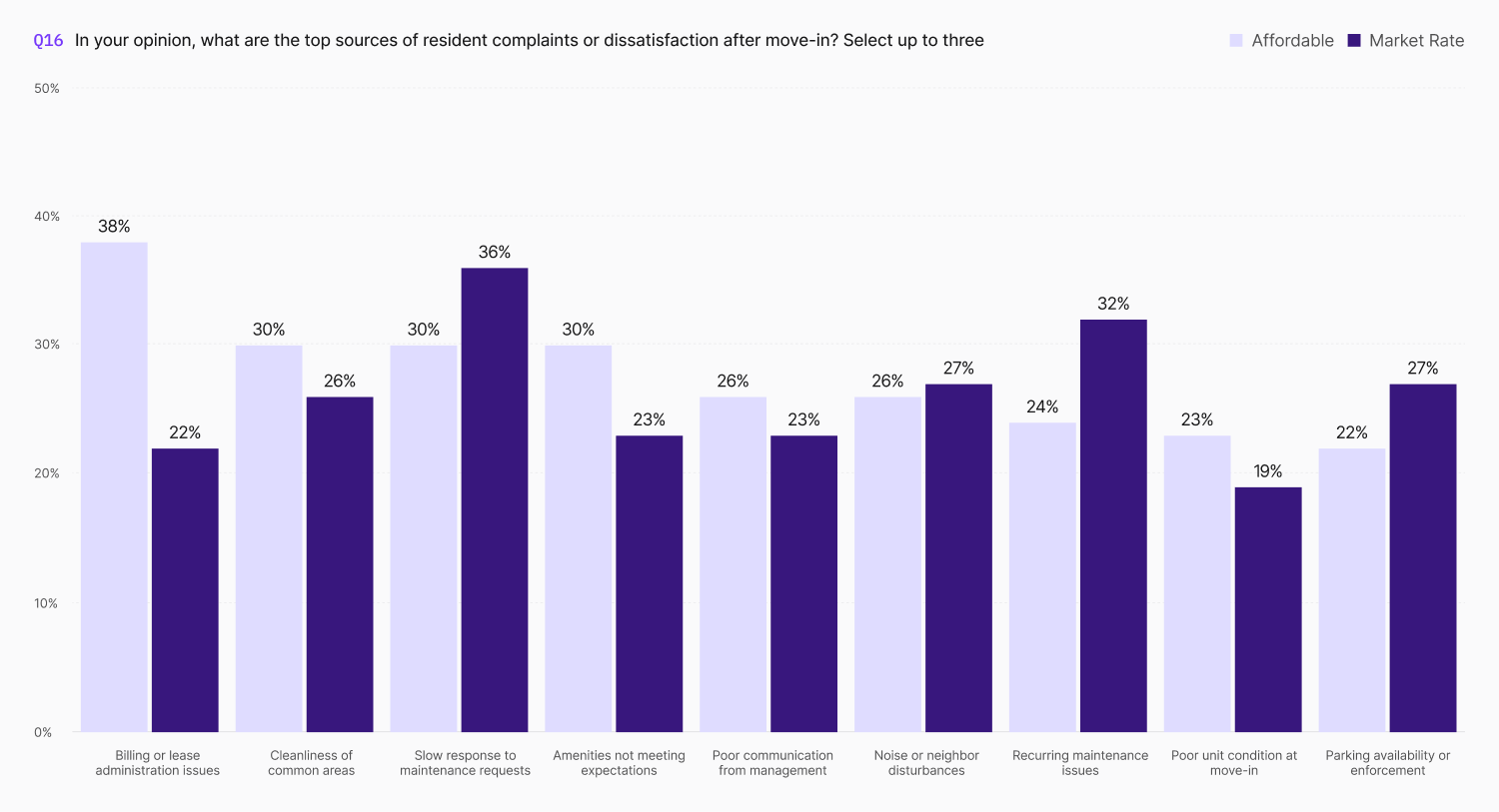

After move-in, the experience gap widens further for affordable renters. Billing and lease administration issues are the number one source of resident complaints for affordable operators at 38%, sixteen percentage points above market rate. That gap is the single largest in the entire survey across all questions, and it reflects a fundamental difference in billing complexity between the two segments. Affordable housing rent calculations involve tenant income portions, HAP payments, utility allowances, and mid-year adjustments tied to income changes and recertification outcomes. Every one of those variables introduces an opportunity for confusion, error, or dispute that simply doesn't exist in a conventional lease where rent is a flat monthly figure.

Maintenance-related complaints, which dominate the market-rate list (36% slow response, 32% recurring issues), rank lower for affordable. This could reflect the AI deployment patterns from Section 2, where affordable operators lead in maintenance AI adoption at 56% vs. 50%. It could also reflect that in the context of affordable housing, billing confusion and administrative complexity are experienced as more immediately frustrating than maintenance timelines.

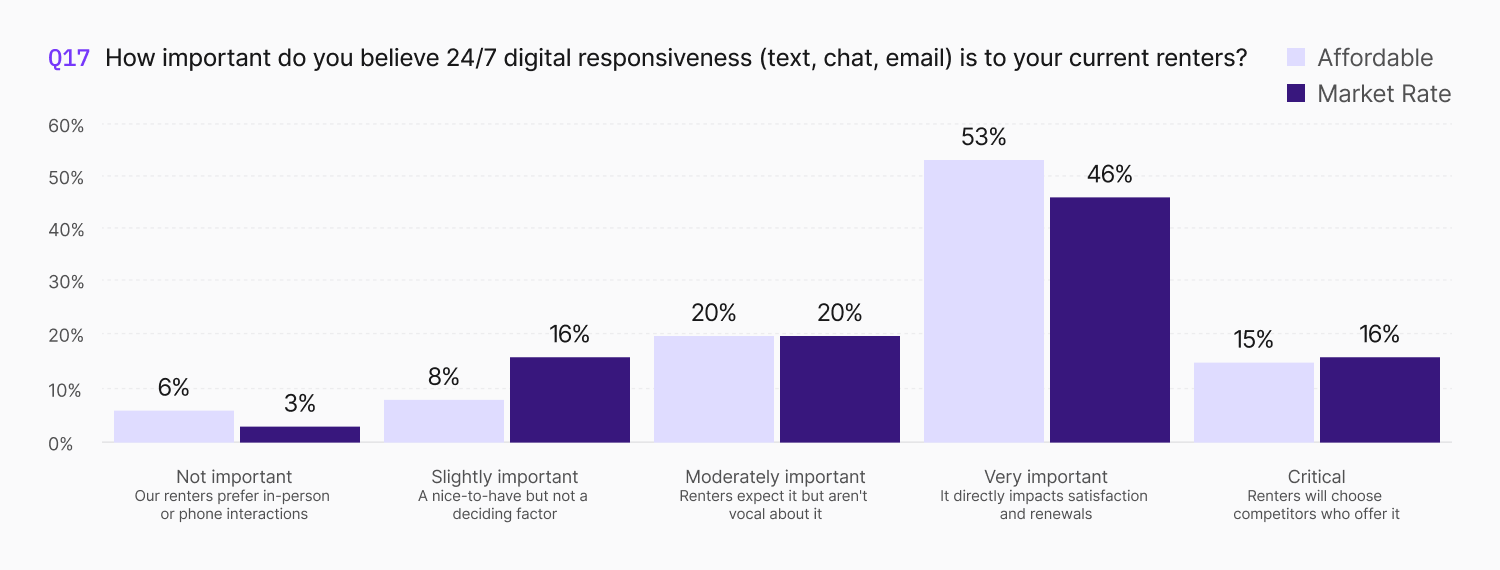

Despite the complexity of their resident populations, affordable operators rate 24/7 digital responsiveness as more important than their market-rate peers. While there's a perception that affordable residents, who may skew older or less digitally native, don't want or need digital communication, the survey suggests operators see it differently. While 6% do note that their renters prefer in-person or phone interactions (double the market-rate figure), the strong majority recognize that digital responsiveness directly impacts satisfaction and retention.

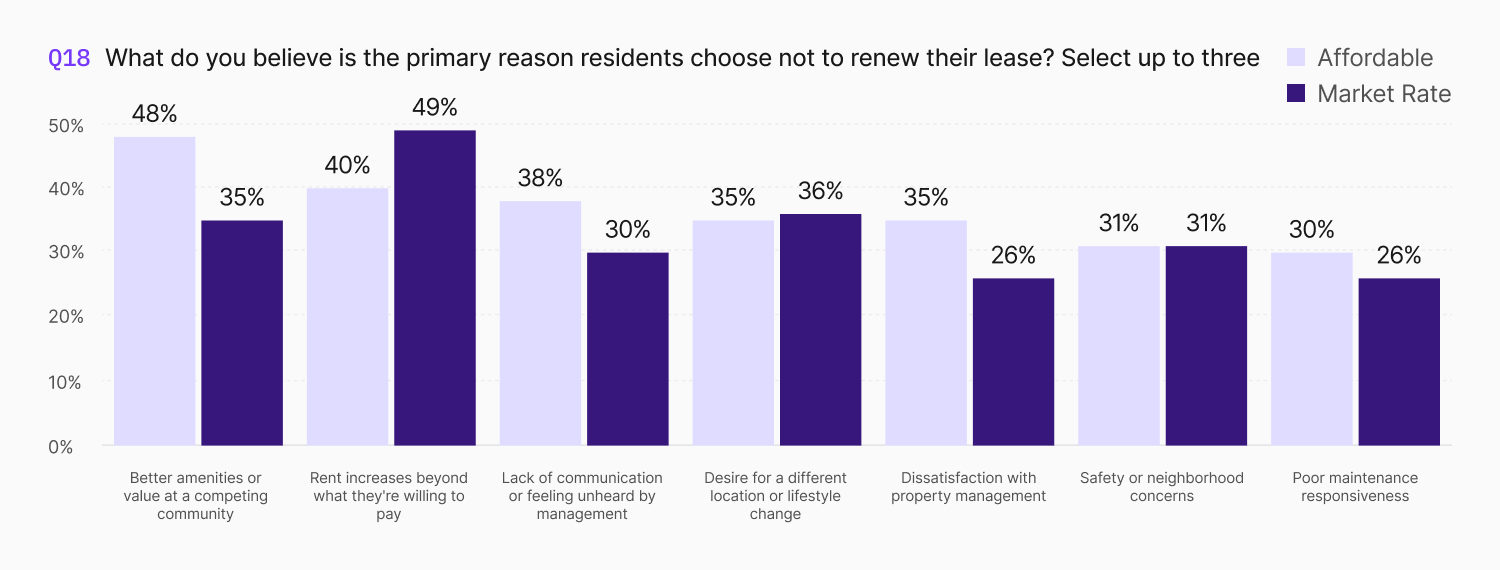

The non-renewal data reveals what's at stake. For market-rate operators, rent increases are the top reason residents leave. For affordable operators, it's losing residents to a competing community that offers better amenities or perceived value, with a delta thirteen points above market rate. The data shows what drives them out is the experience: feeling unheard by management, dissatisfaction with how the property is run, or the perception that a competing community is simply better managed.

This reframes the resident experience conversation for affordable operators. Retention, rather than a pricing conversation, becomes an operations and communication exercise. The properties that invest in responsive communication, streamlined administration, and proactive maintenance are the ones holding onto residents who might otherwise go elsewhere for perceived greener pastures.

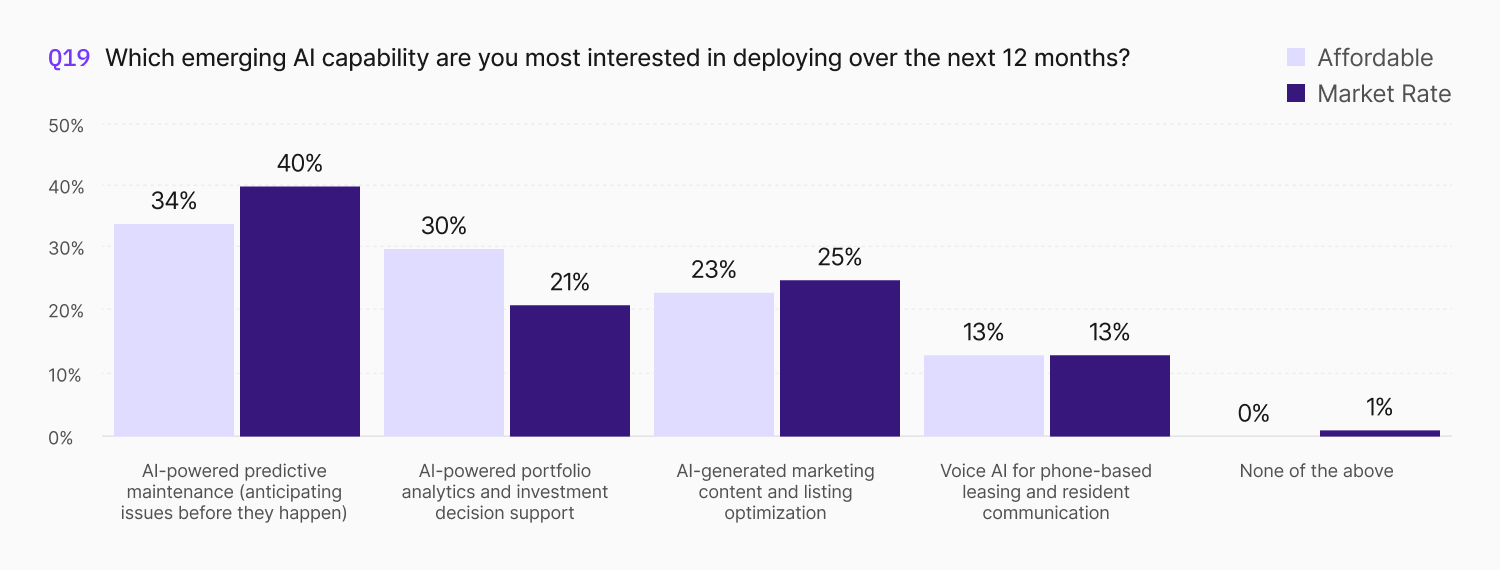

With core AI deployment well underway across leasing, maintenance, and renewals, operators are already looking at where the technology goes next. Predictive maintenance leads the list for both segments. But the more interesting signal for affordable operators is portfolio analytics and investment decision support, where affordable outpaces market rate by nine percentage points.

That gap reflects the increasing sophistication of affordable housing portfolios. Operators managing across LIHTC, HUD, Section 8, and state-financed programs are tracking compliance deadlines, subsidy expirations, capital needs, and regulatory changes across dozens or hundreds of properties simultaneously. The appeal of AI that can surface portfolio-level risk, flag upcoming recertification bottlenecks, or model the financial impact of regulatory changes is readily apparent.

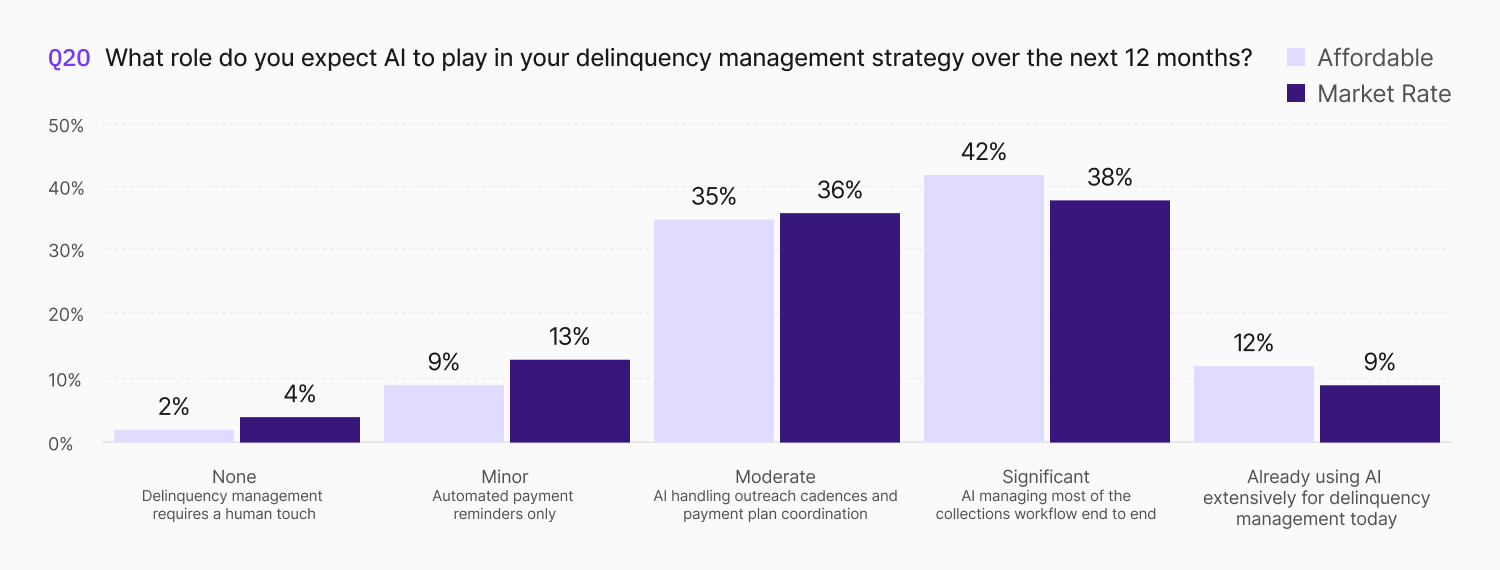

Delinquency in affordable housing carries weight that goes beyond lost revenue. Unpaid balances can trigger compliance complications, affect HAP payment reconciliation, and in severe cases jeopardize a property's standing with its funding agency. The collections process also involves residents who may be experiencing genuine financial hardship, which means outreach cadences, payment plan offers, and escalation protocols need to be handled with both consistency and sensitivity. Operators are betting that AI can manage the routine outreach and coordination at scale while routing the cases that need human judgment to staff who have the capacity to handle them thoughtfully.

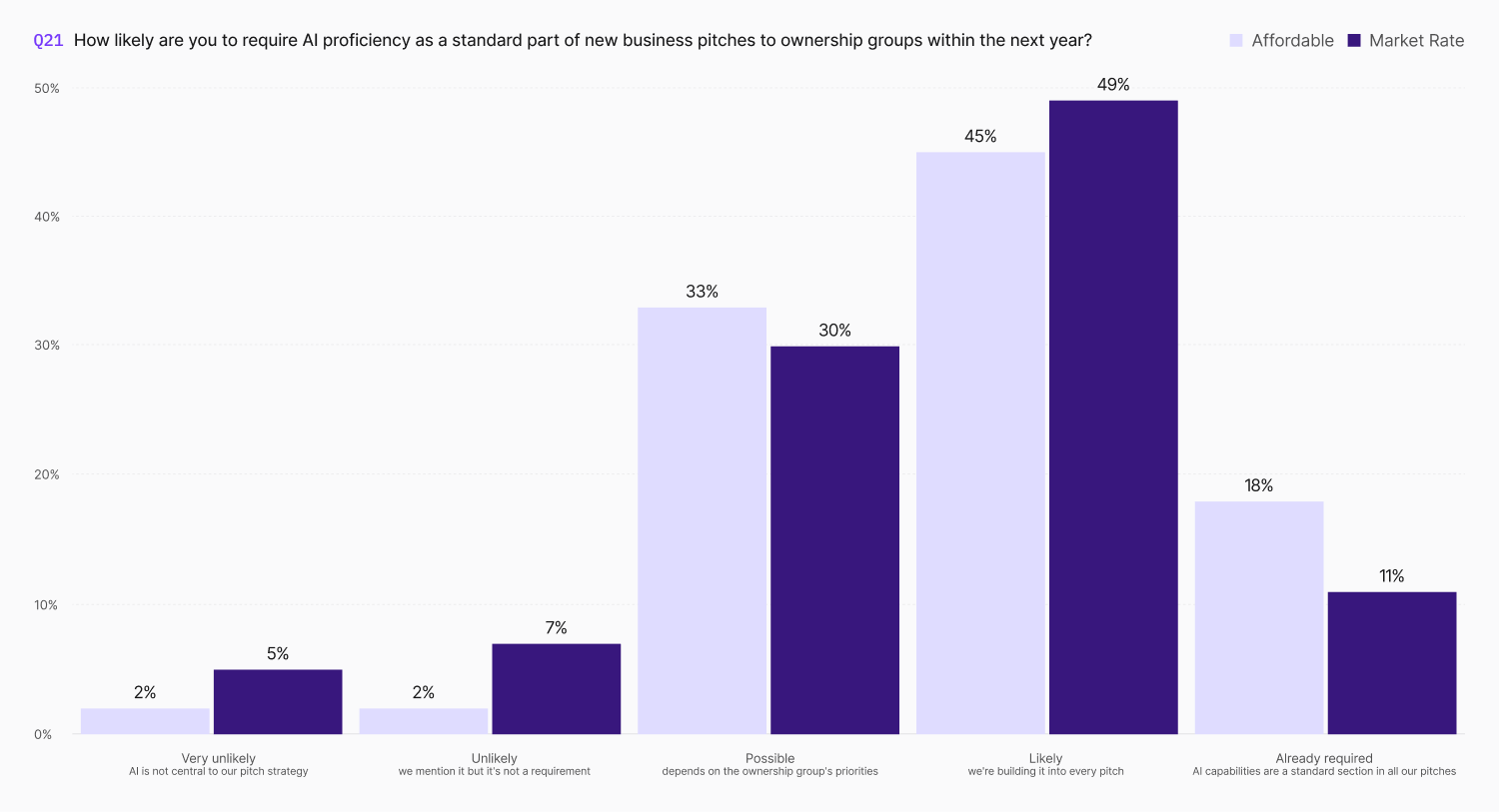

The clearest indicator of where the industry is headed may be what operators are telling ownership groups. 63% percent of affordable operators say AI proficiency is likely or already required as a standard part of new business pitches, and 18% say it's already a required section in every pitch they make. On the other end, only 4% of affordable operators say AI is unlikely to be part of their pitch strategy, compared to 11% of market-rate operators.

For affordable operators, this shift has specific implications. The management companies that can demonstrate AI-driven compliance capabilities, supported by audit trails and measurable outcomes, are positioning themselves for a competitive advantage in winning and retaining affordable portfolios.

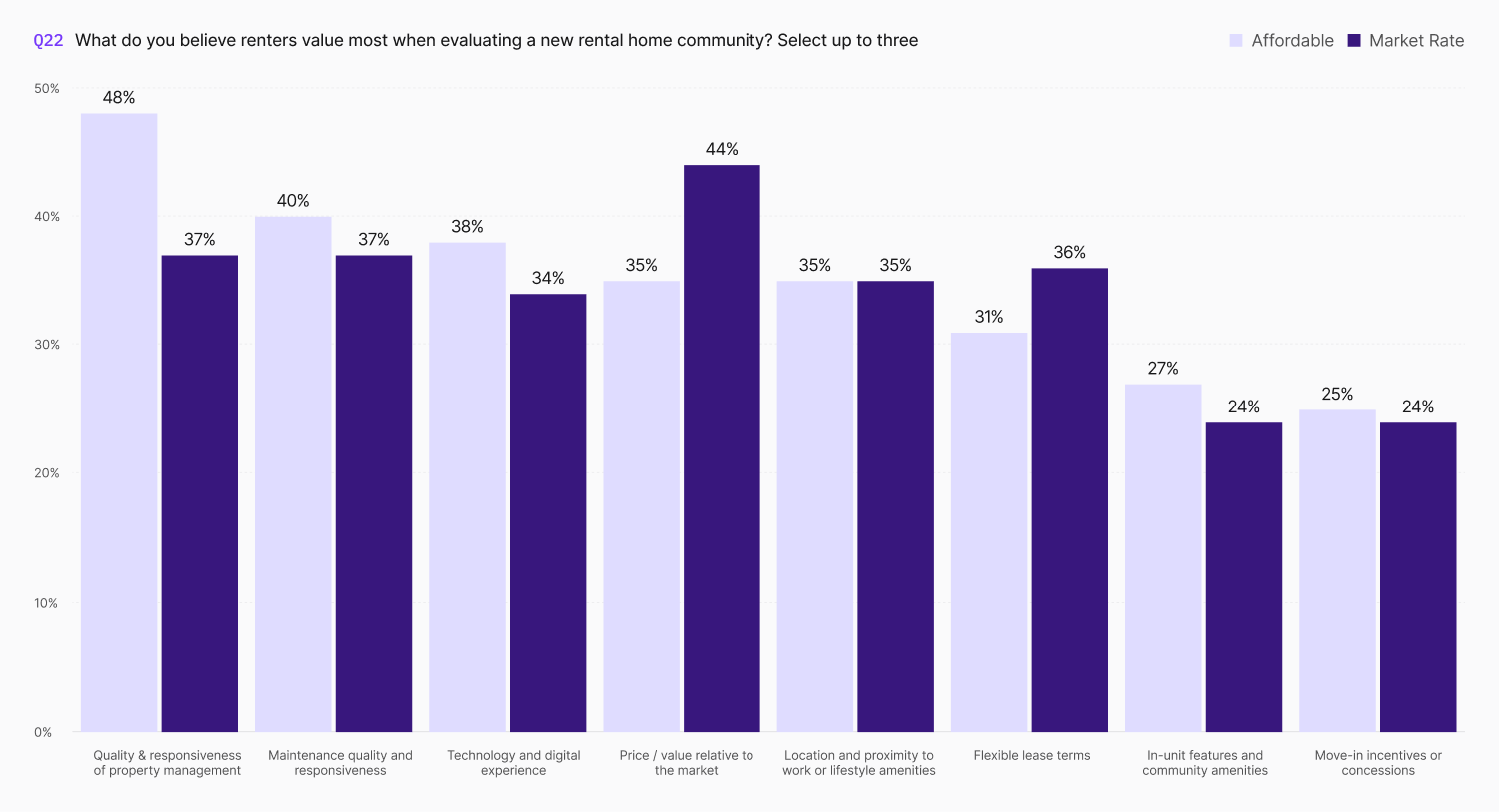

We'll close with what ties this all together. When affordable operators were asked what residents value most when choosing a community, management quality and responsiveness came first, eleven points above market rate.

This is the through line of the entire report. Affordable housing residents are choosing where to live based on how well a property is managed, how responsive the team is, and how modern the experience feels. The operators who recognize this are investing in AI across the resident lifecycle, restructuring their teams to focus human attention where it matters most, and building the compliance and operational infrastructure that allows them to deliver a better experience at scale. The ones who move fastest will define what affordable housing operations look like for the next decade.

The AI adoption question is closed. 91% percent of the affordable operators we surveyed have implemented at least one AI solution into their daily operations, matching adoption rates across their convention peers. 7% of affordable respondents have plans to implement AI within 12 months and only 2% say they have no plans to implement AI at all. What's worth noting is the pace of that adoption. 44% percent of affordable operators report partial deployment, with another 35% fully deployed, suggesting the industry has moved past the pilot phase and into operationalization. The question is no longer about deploying AI in Affordable, it’s where and what gaps remain?

The investment on AI tells the same story. 72% percent of affordable operators are increasing their AI investment by 10% or more year over year, with more than a quarter committing to increases above 25%. The increasing budget allocation indicates that both affordable and market-rate operators are treating AI as core infrastructure, allocating dedicated budgets, planning multi-year rollouts, and embedding these tools into how they staff, train, and evaluate performance.

How that budget gets allocated gives us insights into the technology preference of affordable housing operators. 58% of affordable operators today are working with two to three specialized AI vendors for different functions, while only 3% rely primarily on their PMS vendor's built-in AI features. The multi-vendor approach reflects a reality of operating in the affordable housing segment: no single platform has yet delivered end-to-end coverage across affordable housing operations, so operators are assembling best-of-breed stacks that layer specialized tools on top of existing base tools. For affordable operators in particular, this creates opportunity and complexity alike. More tools means more integration work, more vendors to manage, and more pressure to ensure continued compliance across a fragmented technology ecosystem.

Across the four core operational areas where AI is being deployed today, affordable operators are keeping pace with or outpacing their market-rate peers in almost all areas. Leasing is the most mature category for AI deployment for both segments, with 56% of affordable operators reporting implementation (within three points of market rate). LeasingAI is the lowest friction starting part, with the biggest opportunity to capture unnurtured leads around the clock. However, many of the most operationally complex workflows in affordable housing, including certification, recertification, managing set asides, and waitlist management, remain painstakingly manual, largely pen and paper.

Maintenance is where affordable begins to pull ahead in overall deployment rates, with 56% of surveyed affordable operators deploying AI for maintenance workflows, compared to 50% of market-rate operators. This arguably reflects the outsized pressure affordable teams face in managing high work order volumes with lean staffing, leveraging AI-powered intake, triage, and routing to keep closure percentages high. Renewals too show near-parity, with affordable trailing slightly at 53% versus 56%.

Delinquency is the category with the most forward momentum. Current implementation of delinquency in affordable sits at 46%, the lowest of the four areas, but 40% of those who haven't deployed here yet say they plan to within 12 months. That makes delinquency the clearest next frontier for AI deployment in affordable housing, a trend we’ll explore further later in this report.

The financial returns are beginning to materialize for the affordable segment. 58% of affordable operators report moderate or significant reductions in operating expenses as a direct result of AI-driven efficiencies, outpacing market-rate operators by seven percentage points. This gap is particularly notable given that affordable operators typically work with tighter margins and less technology budget. The fact that they're seeing stronger expense reductions suggests that the operational baseline they're automating away from was more labor-intensive to begin with. When the starting point involves manual recertification tracking, paper applications, and spreadsheet-based compliance workflows, even targeted automation can help to deliver outsized returns.

Confidence levels tell a similar story. Nearly three-quarters of affordable operators say they are very or fully confident that their AI tools will perform effectively during peak leasing season, with 32% saying AI now outperforms their previous manual processes at scale. That seven-point confidence gap over market-rate peers likely reflects what happens when AI replaces processes that were already running past capacity. When your baseline is a small team managing compliance, leasing, and resident communication across hundreds of units, the performance bar AI needs to clear looks different than it does for a fully staffed conventional property. Affordable operators are seeing strong results because the need was that much more acute.

The previous section showed that affordable operators are adopting AI at rates that match or exceed market rate across leasing, maintenance, renewals, and delinquency. But when we ask what's holding them back from going further, some affordable-specific barriers come into focus.

Data privacy and compliance concerns top the list for affordable operators at 44%, seven points above that of their market-rate peers. Affordable operators are astutely asking what data are these models accessing, where is it stored, who reviews the output, and how does the audit trail hold up under a state agency review or HUD inspection.

The second notable gap is onsite team resistance, where affordable operators are 11 percentage points more likely to cite it as a barrier than market-rate operators (29% vs. 18%). This is less about whether staff want new technology to reduce their workload (they do) and more about the conditions under which they're being asked to adopt it (with the aforementioned regulatory complexity). Affordable housing site teams are smaller, and usually carry broader responsibilities across compliance, leasing, and resident services simultaneously. Layering a new tool into an already overloaded workflow creates friction that a larger, more specialized market-rate team may not experience in the same way. The path to adoption starts and ends with thoughtful implementation processes that both account for existing staff capacity and the complexity of the work they're already managing.

Where the data gets interesting is integration challenges. Market-rate operators rank this as their top barrier at 40%, while affordable operators place it lower at 28%. Our hypothesis? Affordable operators, many of whom are still running manual or spreadsheet-based processes for compliance work, have less existing automations to integrate against. The integration challenge assumes you have systems to connect, which, given the budgetary constraints of the affordable segment, often results in less digital infrastructure.

One of the largest gaps in our entire survey between market rate and affordable is about regulatory risk. 46% of affordable operators say they are very concerned or already impacted by AI-related regulatory changes versus 32% of market-rate operators. This 14% gap is the second widest across every question we asked. 15% of affordable operators noted that current regulations are already affecting their AI deployment (roughly two and a half times the market-rate figure), showing the increased compliance focus is already manifesting itself in tech rollouts.

Affordable housing compliance across programs like LIHTC, HUD Section 8, HOME, and Bond demands AI that is auditable, explainable, and defensible under review. The addition of staggered HOTMA implementation requires configurable tools that can manage changing guidance. Most AI tools were not built to manage the layered, ever-changing complexities in affordable housing.

The opportunity this presents is significant. Income certification and recertification are where the most staff time goes and where errors are most expensive, with the potential for loss of millions of dollars in tax credits for a few clerical errors. The operators who close this gap first will outperform on efficiency in ways leasing automation alone can’t deliver. The question is what tool to choose that is built for affordable operators in mind, and how to deploy them properly.

While overall concern levels about new supply are similar across both segments (56% vs. 53% moderately or very concerned), the nature of that concern differs. 9% of affordable operators say they are already seeing downward pressure on rents from oversupply, 3x the market-rate figure. This likely reflects localized LIHTC markets where recent tax credit allocations have concentrated new affordable supply, creating competition among affordable communities in ways that mirror what market-rate operators experience more broadly. In these markets, operational efficiency and resident experience become competitive differentiators in ways they historically haven't been for affordable housing.

Insurance is adding another layer of financial pressure. Half of affordable operators expect significant or severe insurance cost increases in 2026, eight points above market rate. And while market-rate operators are more concentrated in the moderate pressure band (42% budgeting for 5–10% increases), affordable operators skew toward the higher end, with 16% bracing for increases above 20%. Seven percent say they're already restructuring operations to absorb insurance cost growth.

Insurance pressure compounds differently in the affordable segment, with revenue constraints from regulatory rent caps, HAP payment schedules, and income-based rent calculations leaving less room to pass costs through to residents. When insurance, utilities, and maintenance costs rise, the only lever most affordable operators have is operational efficiency. That reality only accelerates the case for automation and AI as a margin preservation strategy.

When asked which operational levers they're pulling in response to these pressures, affordable operators are leaning into technology and efficiency at higher rates than their market-rate peers. 51% are prioritizing operating expense reduction through technology and automation, six points above market rate. Only 4% of affordable operators say they're holding steady with no significant strategic changes. The vast majority are actively adjusting how they operate, and technology is central to that adjustment.

More than half of affordable operators have restructured onsite teams or centralized operations around AI, 10% points above market rate, and this number is expected to grow. The staffing pressure predates AI: lean teams, persistent turnover, and compliance work that makes every new hire expensive. AI provided the mechanism to act on pressure that had been building for years. Routine tasks move to AI so that staff can focus on compliance reviews, hardship conversations, agency reporting.

The after-hours data illustrates what this restructuring looks like in practice. 81% of affordable operators report that AI has delivered moderate to transformative improvement in their ability to respond to prospect inquiries outside business hours, 10 points above market rate. Nearly half say that almost all after-hours inquiries are now resolved by AI without staff involvement. This matters disproportionately in affordable housing. Properties with smaller teams and no dedicated after-hours staff were historically dark from 5 PM to 9 AM. AI has effectively extended the operating hours of affordable properties without adding payroll.

Despite similar AI adoption rates, affordable housing operators consistently report higher challenge levels across resident complaints (38% vs. 29%), managing renewals (35% vs. 26%), and maintenance requests (34% vs. 28%). Automation has not erased the gap because the work is structurally more complex.