Built to Automate & Scale Your Operations

Answer a couple of questions and we'll connect you with the right team member.

Answer a couple of questions and we'll connect you with the right team member.

Of Canadian operators have fully deployed an AI solution into daily operations

Of Canadian operators with AI have been able to reduce operating expenses through their use of it

Of Canadian operators cite a lack of expertise managing AI tools as a top blocker to expanding usage

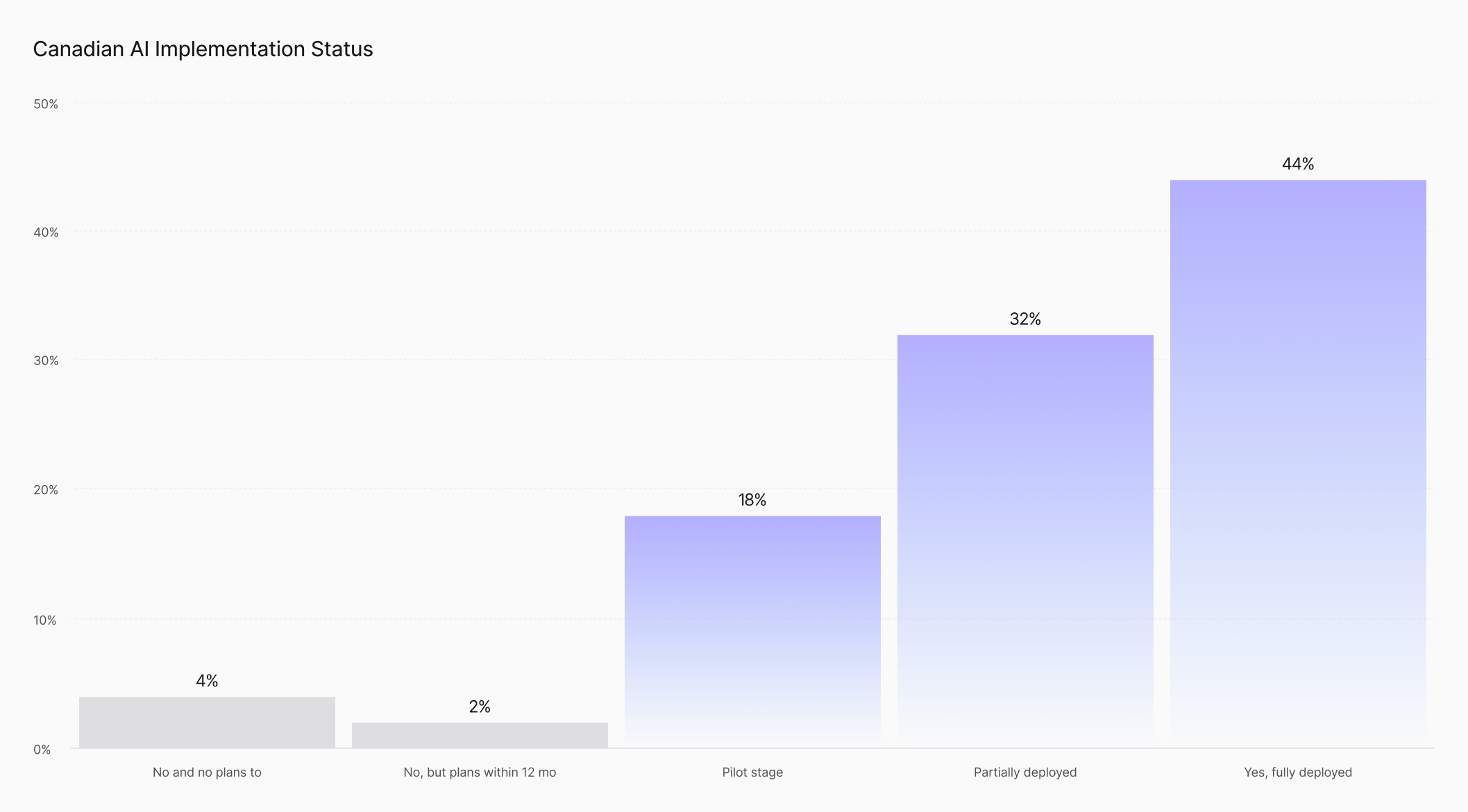

This report draws on a third-party survey of 50 Canadian multifamily decision-makers, conducted as part of a broader study of 400 operators and 700 renters across North America. Across that Canadian sample, only 44% of Canadian multifamily operators have fully deployed an AI solution into their daily operations. The other 56% are still in earlier stages of adoption, either in a pilot, partially deployed, planning to deploy, or have no plans at this time.

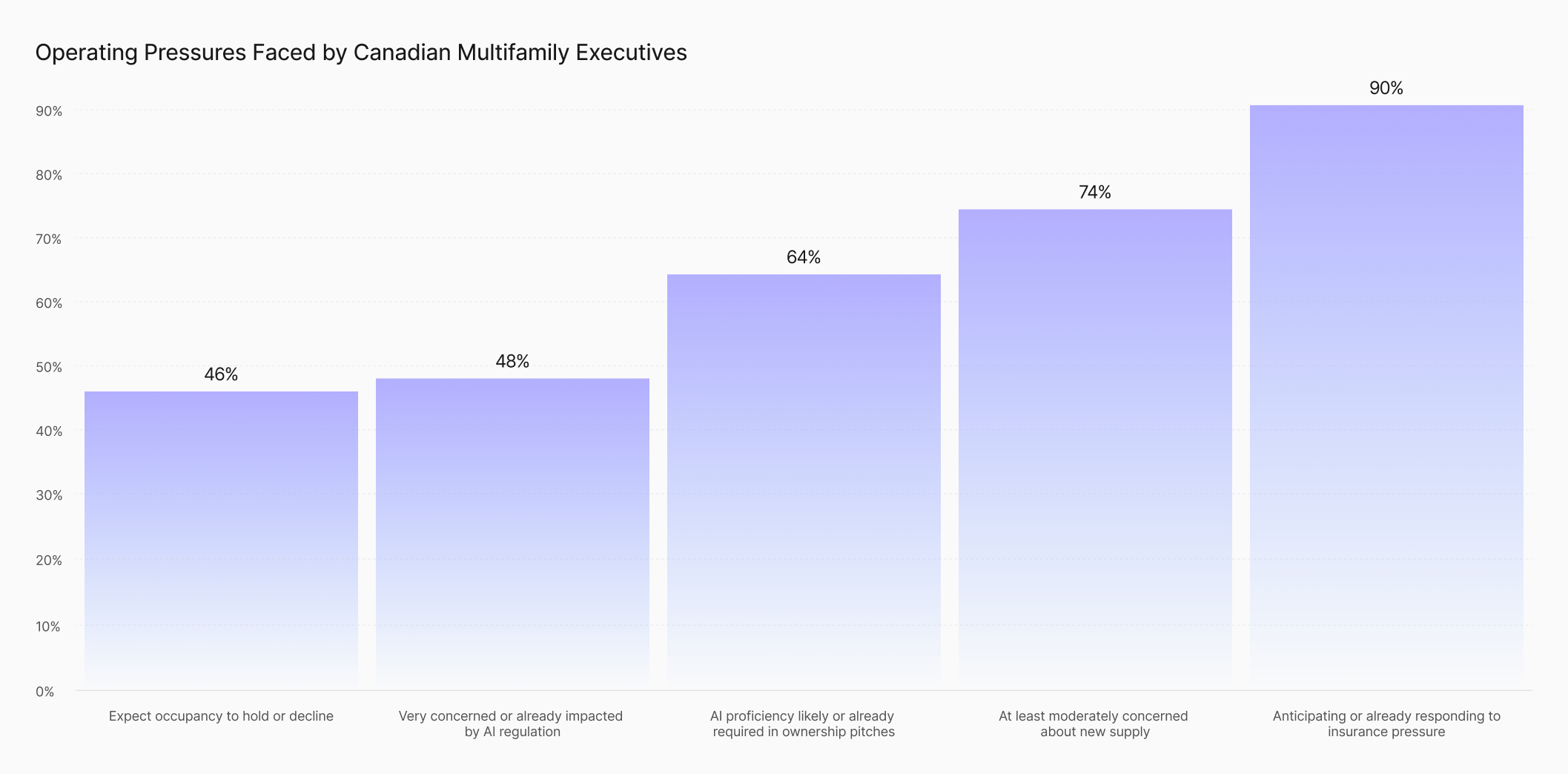

While the majority have yet to fully deploy AI, operators report that AI-driven efficiencies theoretically should matter more in today's macroeconomic environment. Margins are being squeezed, with 90% of operators expecting increased insurance pressure this year, 74% concerned about new supply weighing on rent prices, and 46% expecting occupancy to hold or decline. Growing renter expectations are also adding to the urgency, as 59% of residents now expect 24/7 responsiveness.

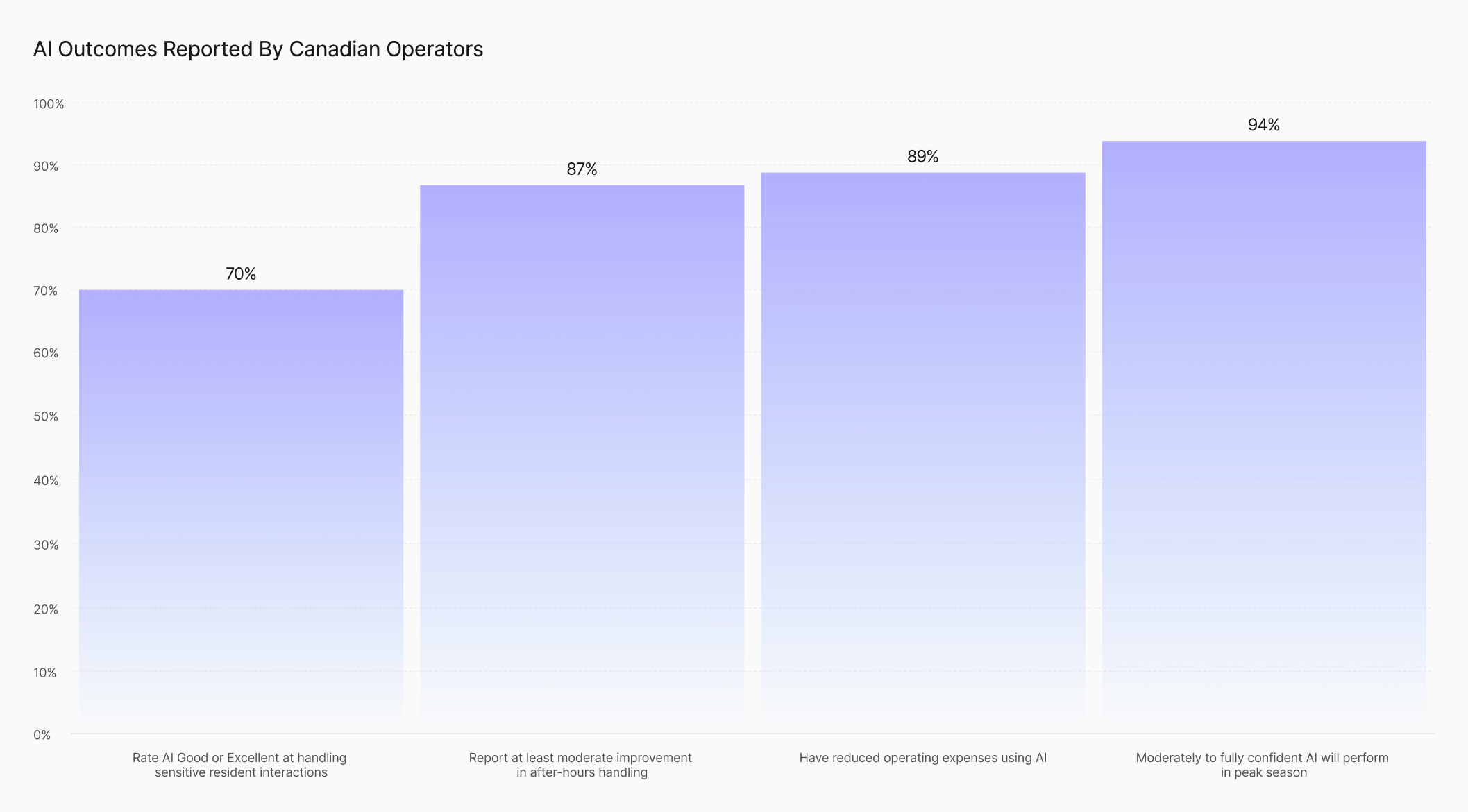

For those who have deployed AI, the technology is showing measurable impact. 89% of operators have been able to reduce operating expenses through their use of AI, 87% report improvements in after-hours prospect management, and 70% rate AI effectiveness in sensitive resident interactions as Good or Excellent. The blocker to expanding AI usage in multifamily does not appear to be the technology.

Instead, Canadian operators name three key barriers to scaling AI further.

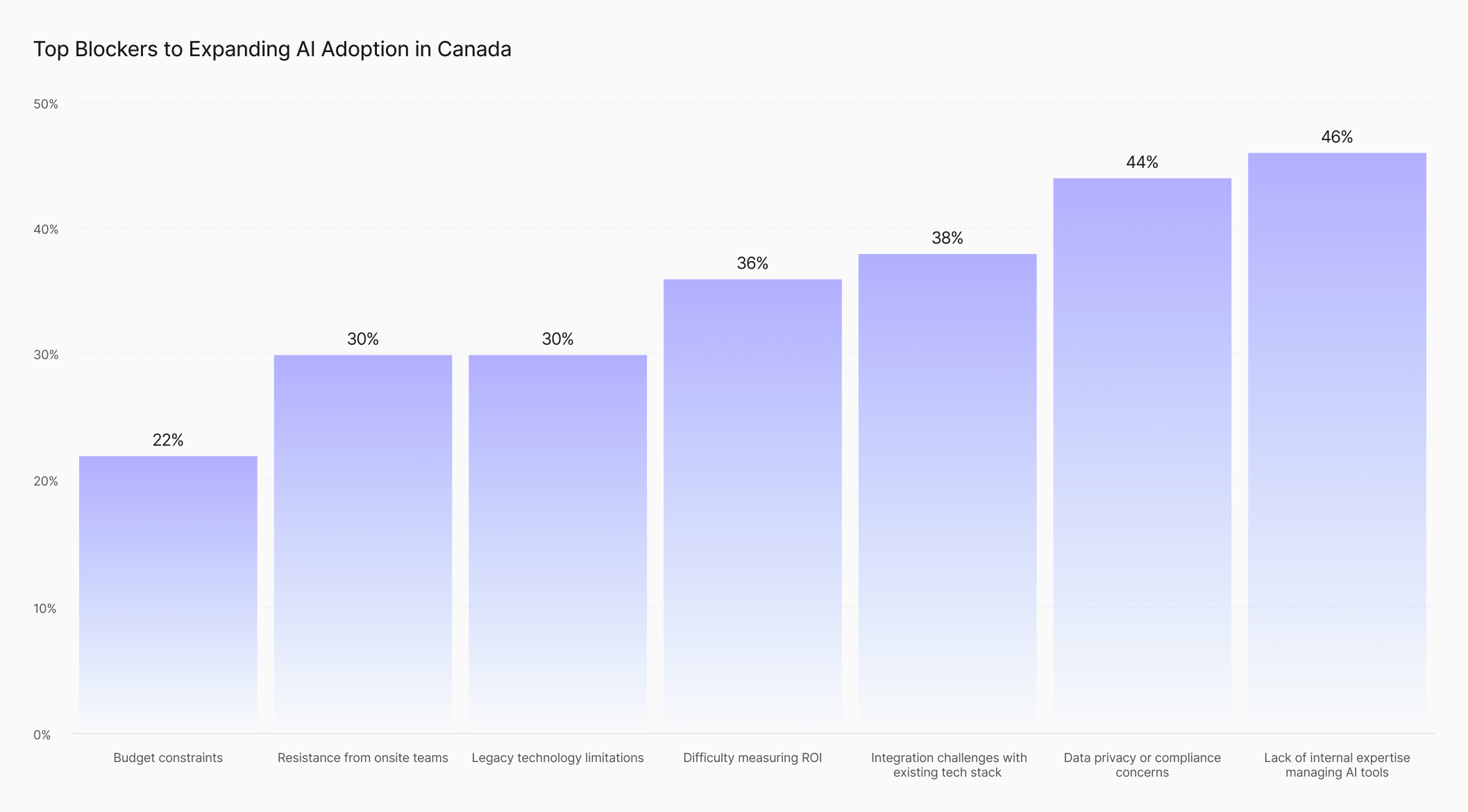

First, internal capability. 46% of operators cite a lack of internal expertise in managing AI as a blocker. The number of AI products available to property managers has grown quickly. As a result, the process of evaluating vendors, leading change management, and building the internal competency to run AI all take capacity most teams don't have to spare.

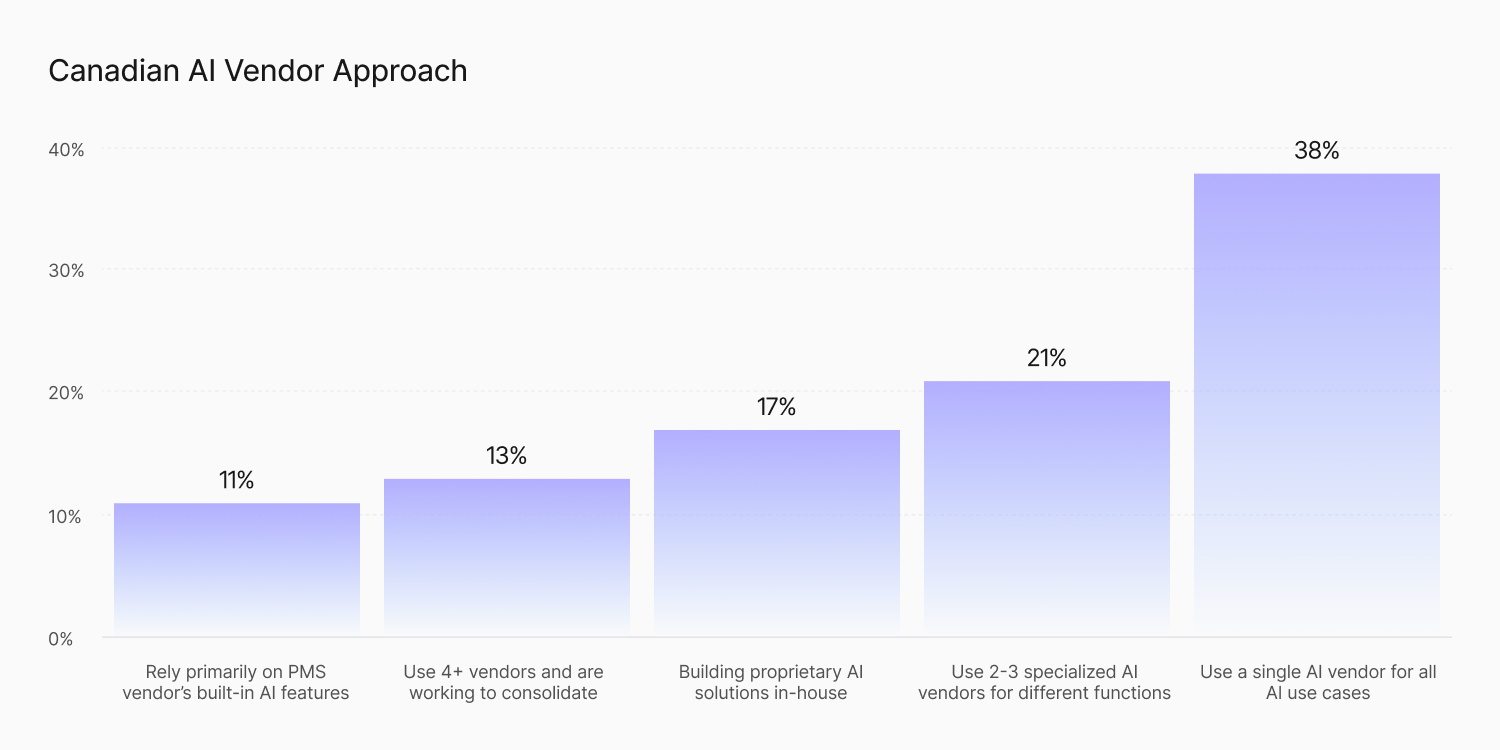

Second, managing integrations across multiple vendors. 38% cite integration challenges as a key blocker. 38% use one AI provider, while 34% use two or more vendors, 11% rely on their PMS for an AI-solution, and 17% are building proprietary AI solutions in-house. The more fragmented the stack, the more complex AI implementation becomes.

Third, data privacy and compliance. 44% of operators cite this as a top barrier to expanding AI usage. The Canadian regulatory landscape is complex, and operators are still working through how AI should handle sensitive resident data in compliance with Canadian laws. This may also contribute to lower AI adoption in delinquency (46%), where the most sensitive information is typically handled.

The combination of macro pressures and rising consumer expectations is driving AI adoption forward despite headwinds, with 94% of operators planning to increase their AI investment in the next year.

This report draws on survey responses from 50 senior leaders at Canadian multifamily companies with over 200 employees, with over half managing portfolios of 1,000 units or more. Most of the Canadian market has introduced AI in some form but less than half have fully deployed it in even one use case.

44% of them reported having fully deployed at least one AI solution into their organization’s daily operations. Another 32% have partially deployed, 18% are in pilot, 2% plan to deploy within the next 12 months, and 4% have no plans at this time.

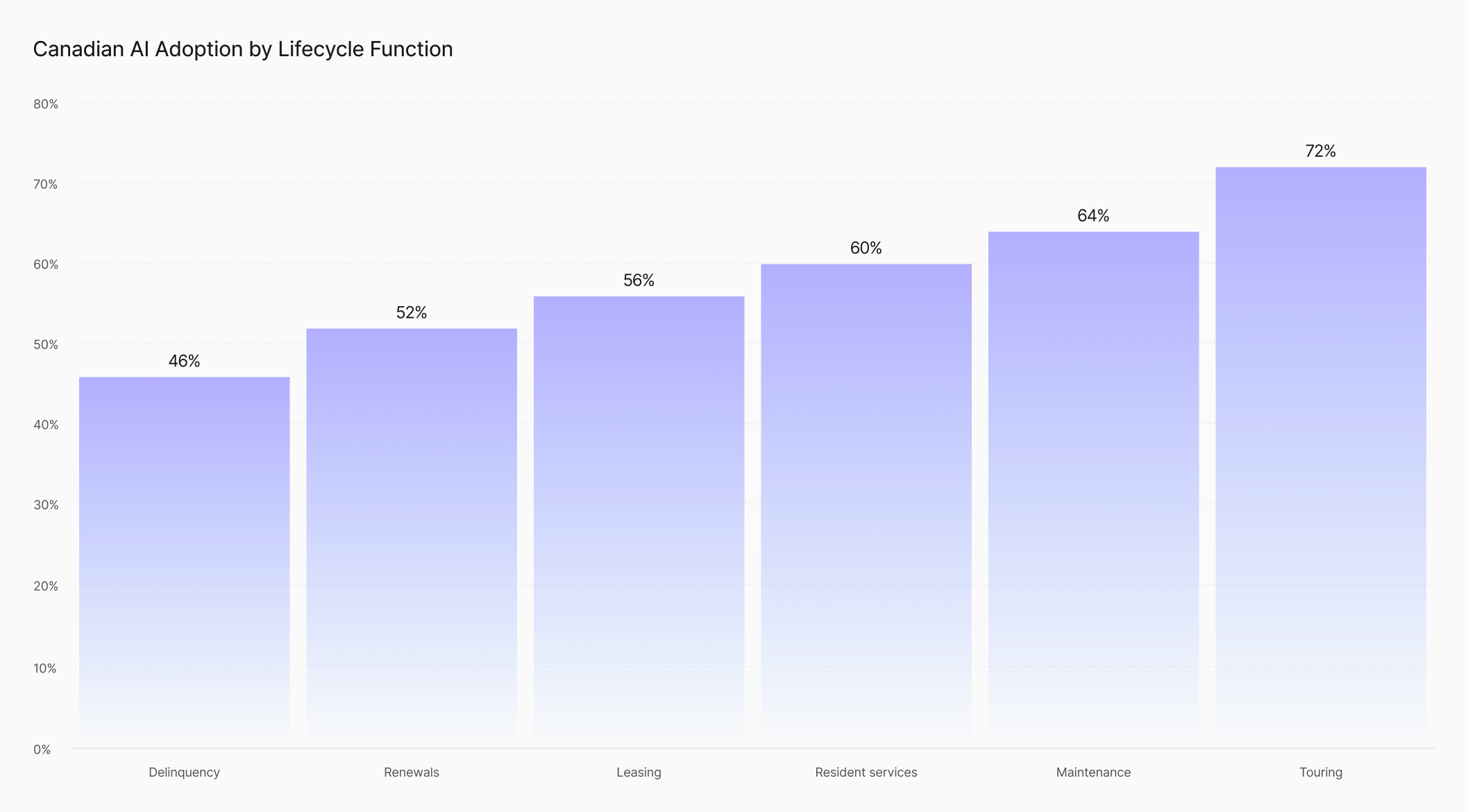

Within those using AI, adoption across the renter lifecycle is uneven. Usage in touring sits at 72% and maintenance at 64%, both areas with high inbound communication volume. From there, it scales down through resident services at 60%, leasing at 56%, renewals at 52%, and delinquency at 46%. Some functions have seen stronger adoption patterns, while others still have significant headroom.

AI is widely introduced, yet full deployment is narrower and fragmented. What's pushing operators to close that gap is the broader 2026 operating environment.

Two forces are putting pressure on Canadian multifamily operations in 2026. First, margins are being compressed from multiple directions, including rising insurance costs, new supply weighing on rents, and softer occupancy. Second, renters are becoming conditioned by other always-on consumer experiences in today’s world. As a result, they’re holding operators to higher standards of responsiveness that onsite teams struggle to meet. Both forces push AI further up the priority list.

Ownership pressure is adding another layer. 64% of Canadian operators say AI proficiency is likely required or already required as a standard part of new business pitches to ownership groups within the next year. For operators without a clear AI strategy, winning new business will get harder.

Margins this year are coming from operations, not rent growth. The operating model has less slack to absorb pressure than it did 12 months ago. AI is the lever many Canadian operators are reaching for to absorb the pressure.

59% of Canadian renters expect 24/7 responsiveness from their property management team. Over three-quarters expect a response to a new inquiry within the same business day, and half expect a response within a few hours. The window for onsite teams to circle back is shrinking.

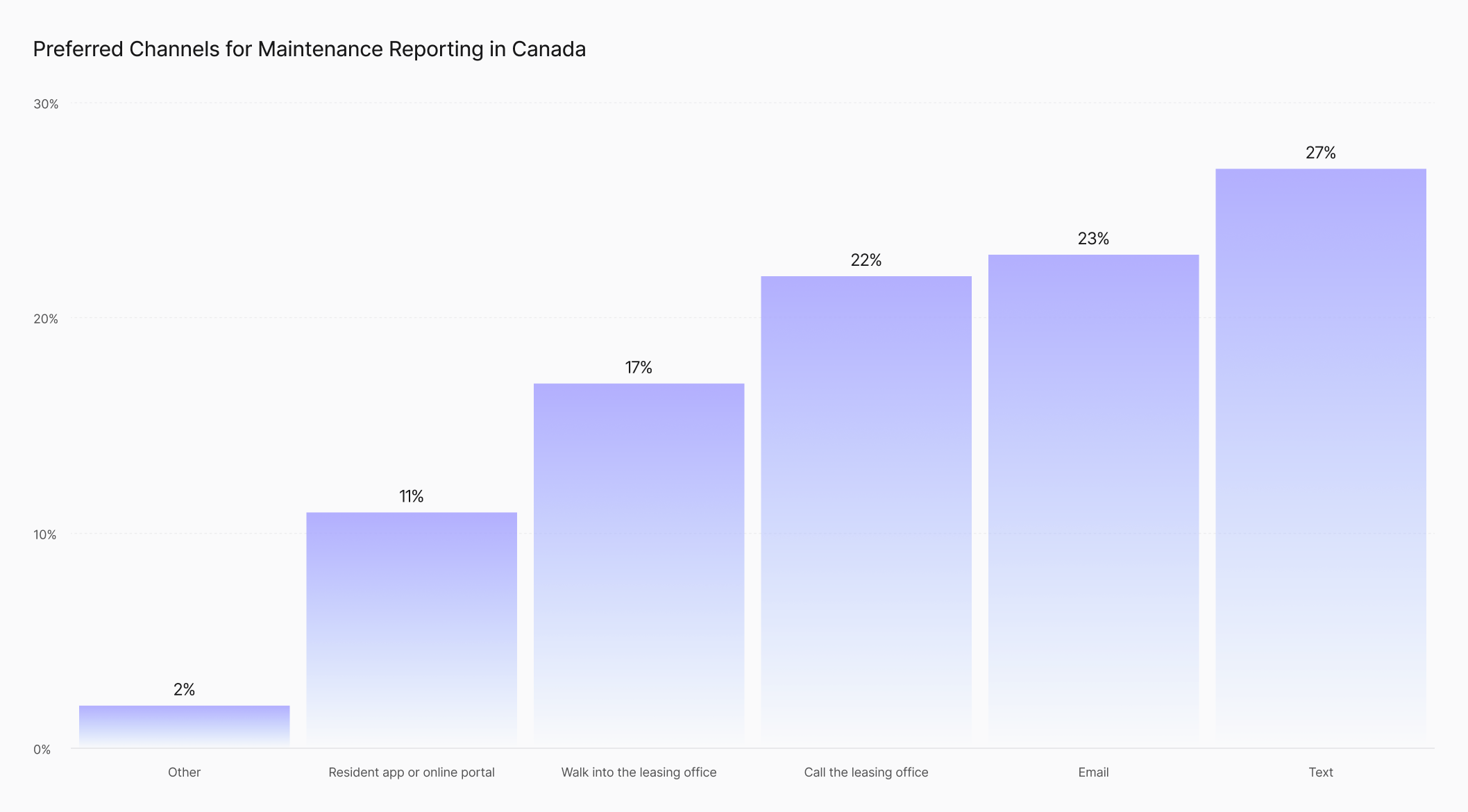

The channel mix matters as much as the speed. When asked how they prefer to report a property maintenance issue, 27% of Canadian renters choose text, 23% email, 22% call the leasing office, and 17% walk in. Only 11% prefer their building’s resident app or online portal. The channels modern AI handles best are the channels renters actually use.

Onsite teams cannot sustain 24/7 coverage across text, email, and phone manually. The operators meeting the expectation are the ones who've deployed AI across the channels renters use. For those operators, the technology is delivering measurable returns.

For the Canadian operators who have committed to AI, the technology is measurably impacting their bottom line.

89% of Canadian operators with AI have been able to reduce operating expenses through their use of it, with half the market seeing reductions in the moderate-to-significant range. There is a real benefit to NOI for the operators who have deployed it.

The same pattern holds in after-hours coverage. 87% of operators using AI for after-hours prospect management report at least moderate improvement, and 19% describe it as a transformative competitive edge. Coverage that previously required inconsistent third-party call centers is now handled 24/7 by customizable and trainable AI solutions.

Operators also have confidence even in the most nuanced interactions. 70% rate AI effectiveness in emotionally sensitive resident interactions as Good or Excellent. Not a single one rated it Poor.

This trust in AI also carries forward into peak season, with 94% of operators saying they are at least moderately confident their AI tools will perform during the busiest stretches of the year.

For Canadian operators who have fully deployed AI, the technology is working. What's holding operators back from scaling it further is not the technology itself, but the operating capability and strategy around it.

When asked about the biggest challenges preventing Canadian operators from expanding or implementing AI across their portfolio, they name three key barriers. Rather than the technology itself, they’re about internal capability, integration challenges, and data privacy and compliance concerns.

46% of Canadian operators cite a lack of internal expertise managing AI as a top barrier to expanding usage. It’s the most-cited barrier in the data, ahead of compliance concerns (44%), integration challenges (38%), and ROI visibility (36%).

The number of AI products available to property managers has grown quickly. Operators now have to evaluate numerous AI vendors, run pilots, lead change management, train onsite teams, and justify the spend to ownership. This requires resources, talent, and internal bandwidth to navigate these changes. The capability gap isn’t about whether operators understand AI conceptually. It’s about whether they have the people and the time to evaluate it, deploy it, and run it well across multiple properties.

A further 36% of operators say their current AI doesn’t give them a clear enough measurement of ROI needed to justify expansion. Operators see AI working in their day-to-day, yet the solutions of many vendors make it difficult to put a defensible number on it when asked. Without a platform and vendor that helps provide clear measurement, the case for expanding gets harder.

38% of Canadian operators name integration challenges with their existing tech stack as another top barrier to expanding AI. Looking at how operators have built out their AI vendor approach explains why.

34% of operators use two or more AI providers. The more fragmented the stack, the more complex the integration becomes, and the more time it requires. This ties back to the capability barrier. Operators trying to manage fragmented stacks are stretched thin on the expertise they’re already missing.

44% of Canadian operators name data privacy and compliance concerns as a top barrier to expanding AI.

The Canadian regulatory environment involves multiple frameworks operators need to work through. PIPEDA, provincial privacy laws, and varying requirements around how resident data is handled all add complexity to AI deployment.

This may also contribute to AI adoption being lowest in delinquency management, which sits at 46% adoption, the lowest of any lifecycle stage. Delinquency is where resident data tends to be most sensitive: financial hardship details, payment histories, and outreach records that operators may handle more cautiously.

These three barriers explain where expansion has stalled. How Canadian operators are working through them shows up in their budgets, staffing decisions, and roadmap signals.

Despite the barriers, our survey indicates Canadian operators are leaning further into AI. Their response to the 2026 operating environment is showing up in their budgets, staffing decisions, and roadmap signals.

First, 94% of Canadian operators are increasing their AI investment year over year. The technology built for multifamily has improved dramatically in recent years, and operators are seeing more and more of their peers adopting AI as a result. Their neighbours across the border are doing so too, as shown in this 2025 U.S. State of AI in Multifamily report.

Operators are also signaling where they’re planning to push AI next. 75% expect AI to play a moderate or significant role in their delinquency management strategy over the next 12 months. 50% expect AI to manage most of the collections workflow end-to-end, 25% expect AI to handle outreach cadences and payment plan coordination, and 17% are already using AI extensively in delinquency workflows. Delinquency sits at the bottom of the current adoption ranking at 46% but is an area operators intend to expand much further.

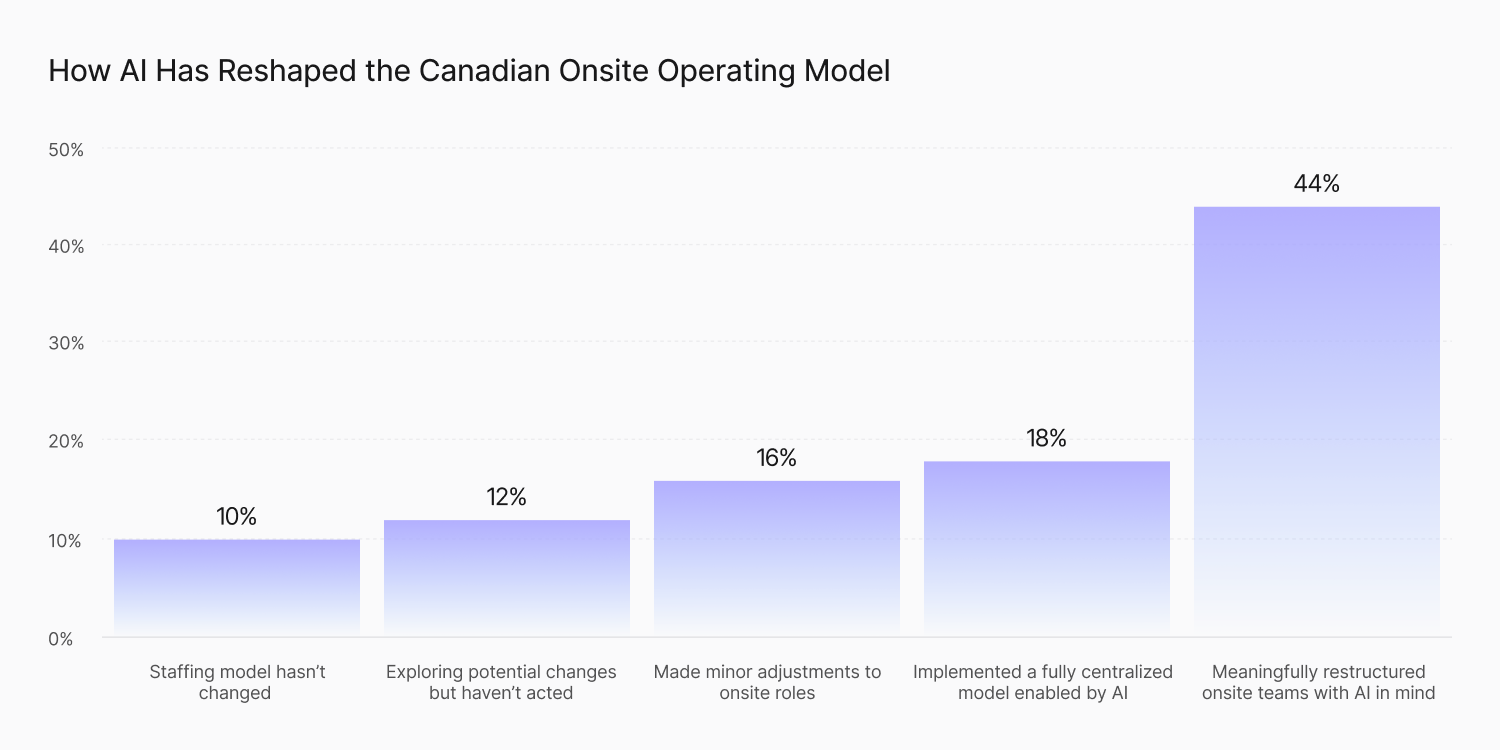

Second, Canadian operators are reimagining their operating model and staffing. 62% of operators said they have either restructured onsite teams around AI or moved to a fully centralized model. 44% have restructured onsite teams with AI in mind, and 18% have implemented a fully centralized model enabled by AI. Another 16% have made minor adjustments, 12% are exploring potential changes but haven’t acted yet, and only 10% have not changed their staffing model at all.

Canadian operators are investing more, restructuring around AI, and consolidating where they can. Over the next 12 months, operators closing the gap between AI introduction and full AI deployment will be able to respond to rising macro pressures and stay ahead of the curve against competitors.

This report draws on a third-party survey of 50 Canadian multifamily decision-makers, conducted as part of a broader study of 400 operators and 700 renters across North America. Canadian operator respondents were senior leaders, including C-suite, at companies with 200 to over 5,000 employees, and over half were at companies with more than 1,000 employees. The renter sample includes 200 Canadian renters across the country. Where the report references operator and prospect conversations, those are treated as supporting color rather than primary evidence. Survey numbers are the source of every quantitative claim in this report.

This report draws on survey responses from 50 senior leaders at Canadian multifamily companies with over 200 employees, with over half managing portfolios of 1,000 units or more. Most of the Canadian market has introduced AI in some form but less than half have fully deployed it in even one use case.

44% of them reported having fully deployed at least one AI solution into their organization’s daily operations. Another 32% have partially deployed, 18% are in pilot, 2% plan to deploy within the next 12 months, and 4% have no plans at this time.

Within those using AI, adoption across the renter lifecycle is uneven. Usage in touring sits at 72% and maintenance at 64%, both areas with high inbound communication volume. From there, it scales down through resident services at 60%, leasing at 56%, renewals at 52%, and delinquency at 46%. Some functions have seen stronger adoption patterns, while others still have significant headroom.

AI is widely introduced, yet full deployment is narrower and fragmented. What's pushing operators to close that gap is the broader 2026 operating environment.

Two forces are putting pressure on Canadian multifamily operations in 2026. First, margins are being compressed from multiple directions, including rising insurance costs, new supply weighing on rents, and softer occupancy. Second, renters are becoming conditioned by other always-on consumer experiences in today’s world. As a result, they’re holding operators to higher standards of responsiveness that onsite teams struggle to meet. Both forces push AI further up the priority list.

Ownership pressure is adding another layer. 64% of Canadian operators say AI proficiency is likely required or already required as a standard part of new business pitches to ownership groups within the next year. For operators without a clear AI strategy, winning new business will get harder.

Margins this year are coming from operations, not rent growth. The operating model has less slack to absorb pressure than it did 12 months ago. AI is the lever many Canadian operators are reaching for to absorb the pressure.

59% of Canadian renters expect 24/7 responsiveness from their property management team. Over three-quarters expect a response to a new inquiry within the same business day, and half expect a response within a few hours. The window for onsite teams to circle back is shrinking.

The channel mix matters as much as the speed. When asked how they prefer to report a property maintenance issue, 27% of Canadian renters choose text, 23% email, 22% call the leasing office, and 17% walk in. Only 11% prefer their building’s resident app or online portal. The channels modern AI handles best are the channels renters actually use.

Onsite teams cannot sustain 24/7 coverage across text, email, and phone manually. The operators meeting the expectation are the ones who've deployed AI across the channels renters use. For those operators, the technology is delivering measurable returns.

For the Canadian operators who have committed to AI, the technology is measurably impacting their bottom line.

89% of Canadian operators with AI have been able to reduce operating expenses through their use of it, with half the market seeing reductions in the moderate-to-significant range. There is a real benefit to NOI for the operators who have deployed it.

The same pattern holds in after-hours coverage. 87% of operators using AI for after-hours prospect management report at least moderate improvement, and 19% describe it as a transformative competitive edge. Coverage that previously required inconsistent third-party call centers is now handled 24/7 by customizable and trainable AI solutions.

Operators also have confidence even in the most nuanced interactions. 70% rate AI effectiveness in emotionally sensitive resident interactions as Good or Excellent. Not a single one rated it Poor.

This trust in AI also carries forward into peak season, with 94% of operators saying they are at least moderately confident their AI tools will perform during the busiest stretches of the year.

For Canadian operators who have fully deployed AI, the technology is working. What's holding operators back from scaling it further is not the technology itself, but the operating capability and strategy around it.

When asked about the biggest challenges preventing Canadian operators from expanding or implementing AI across their portfolio, they name three key barriers. Rather than the technology itself, they’re about internal capability, integration challenges, and data privacy and compliance concerns.

46% of Canadian operators cite a lack of internal expertise managing AI as a top barrier to expanding usage. It’s the most-cited barrier in the data, ahead of compliance concerns (44%), integration challenges (38%), and ROI visibility (36%).

The number of AI products available to property managers has grown quickly. Operators now have to evaluate numerous AI vendors, run pilots, lead change management, train onsite teams, and justify the spend to ownership. This requires resources, talent, and internal bandwidth to navigate these changes. The capability gap isn’t about whether operators understand AI conceptually. It’s about whether they have the people and the time to evaluate it, deploy it, and run it well across multiple properties.

A further 36% of operators say their current AI doesn’t give them a clear enough measurement of ROI needed to justify expansion. Operators see AI working in their day-to-day, yet the solutions of many vendors make it difficult to put a defensible number on it when asked. Without a platform and vendor that helps provide clear measurement, the case for expanding gets harder.

38% of Canadian operators name integration challenges with their existing tech stack as another top barrier to expanding AI. Looking at how operators have built out their AI vendor approach explains why.

34% of operators use two or more AI providers. The more fragmented the stack, the more complex the integration becomes, and the more time it requires. This ties back to the capability barrier. Operators trying to manage fragmented stacks are stretched thin on the expertise they’re already missing.

44% of Canadian operators name data privacy and compliance concerns as a top barrier to expanding AI.

The Canadian regulatory environment involves multiple frameworks operators need to work through. PIPEDA, provincial privacy laws, and varying requirements around how resident data is handled all add complexity to AI deployment.

This may also contribute to AI adoption being lowest in delinquency management, which sits at 46% adoption, the lowest of any lifecycle stage. Delinquency is where resident data tends to be most sensitive: financial hardship details, payment histories, and outreach records that operators may handle more cautiously.

These three barriers explain where expansion has stalled. How Canadian operators are working through them shows up in their budgets, staffing decisions, and roadmap signals.